Thought that title may have gotten your attention.

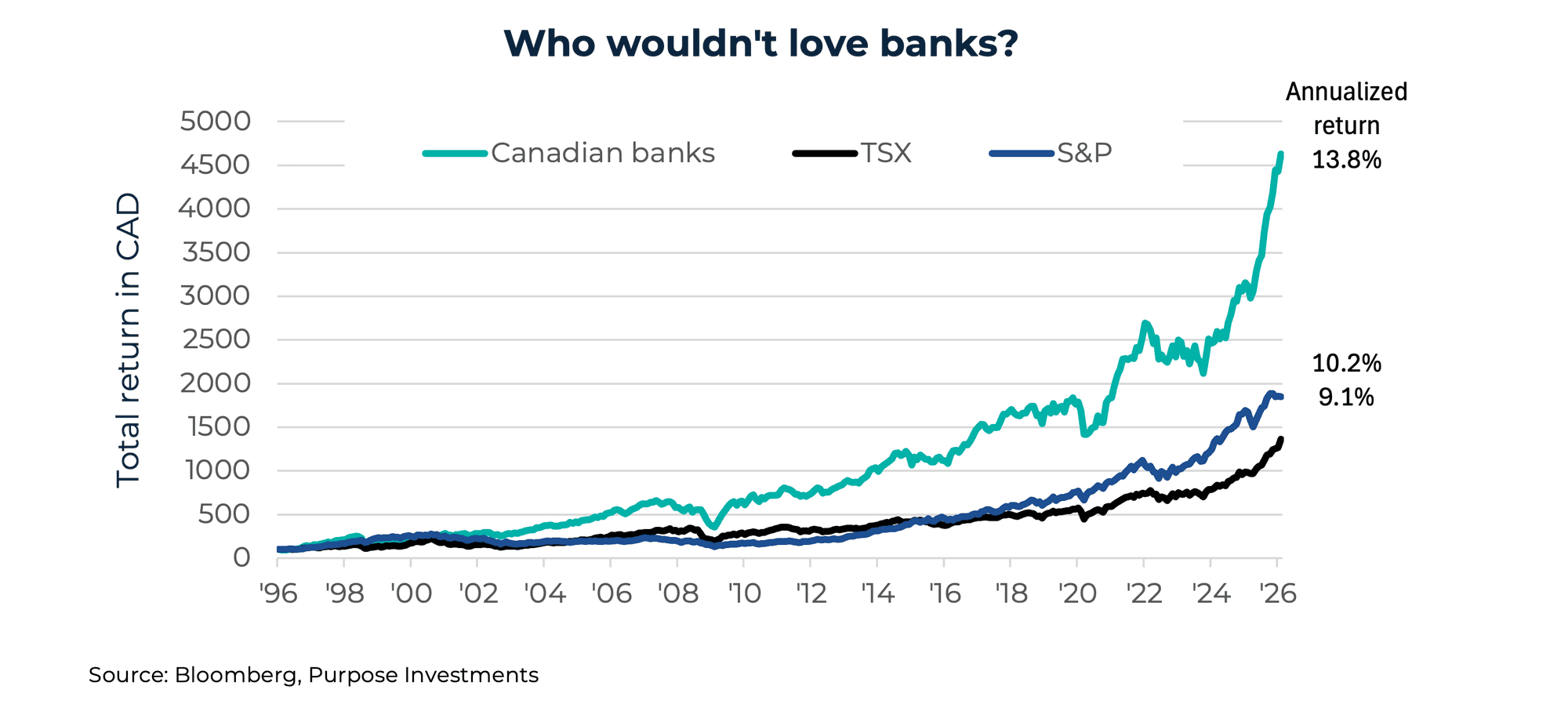

To be clear, we’re talking about the epic performance run of bank stocks over the past decades, not a rush of customers trying to get back their deposits. Over the past 30 years, Canadian banks have earned annualized returns of 13.8%. That’s better than the overall TSX at 9.1%, and even better than the almighty S&P 500 at 10.2%. It’s little wonder Canadians have a soft spot in both their hearts and portfolios for Canadian banks.

Last year, too, banks crushed it, growing 45% based on S&P/TSX Banks index. Sure, gold got most of the attention for helping drive the TSX to an overall 30% gain for 2025, but banks deserve about equal credit.

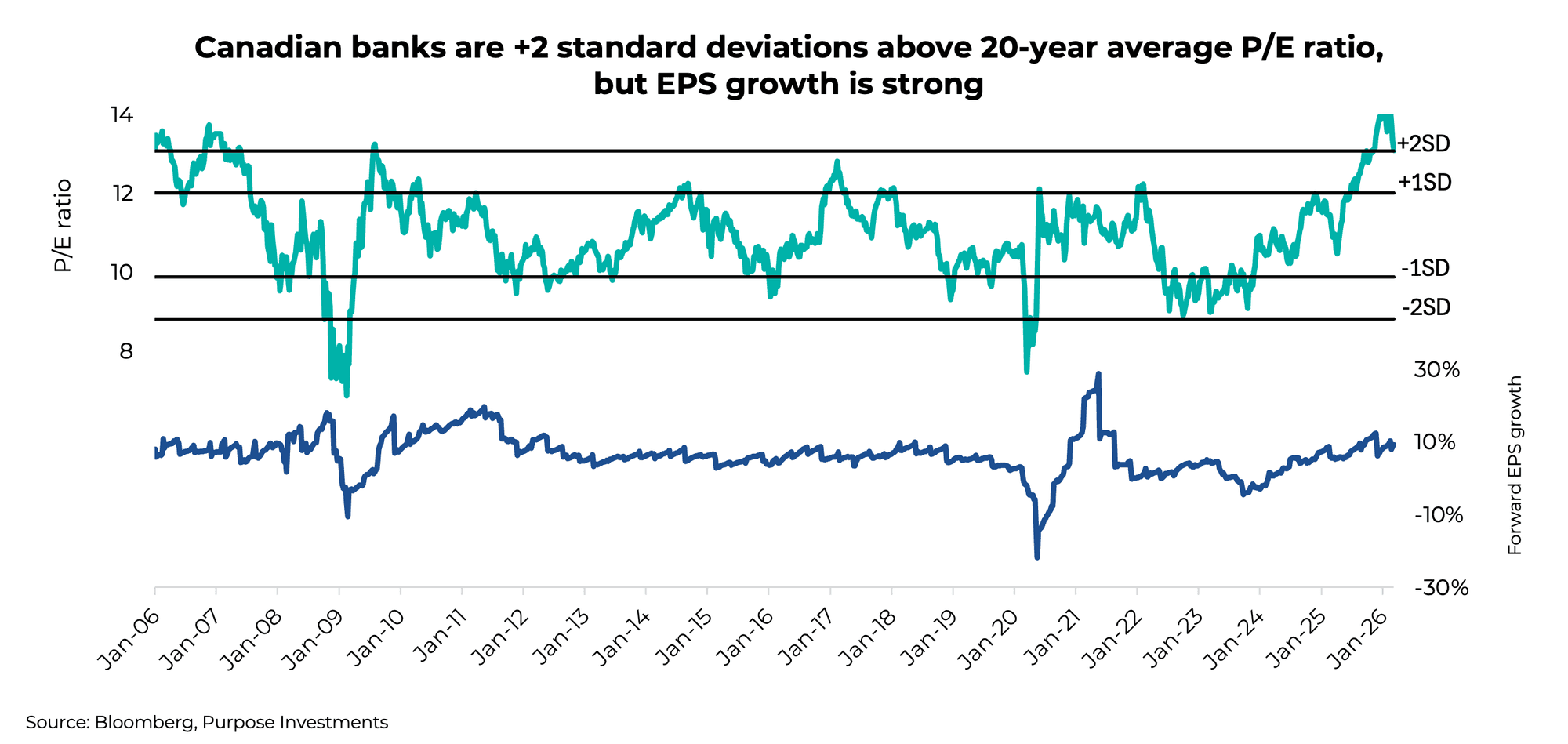

Here’s the challenge, though: bank valuations have certainly been pushed higher. The chart below is the Canadian bank index over the past 20 years. The price-to-earnings ratio was 14x in February, but it has moderated down to 13.1x today. For the banks, that’s pretty pricey.

Valuations are just one part of the story, as earnings growth somewhat justifies the higher valuations. Earnings estimates have been on the rise for the banks, and current forecasts have earnings growing at just under 10% looking out over the next 12-month period. Still at 13.1x, investors are certainly paying up for this growth.

Banks are feeling some tailwinds that have driven share prices higher. Net interest income is strong thanks to higher yields, and loan losses remain contained. Plus, capital markets and wealth are doing well, while housing and real estate are a bit of a laggard. With the rise in share prices, how much of the good news is already priced in? We would say a healthy amount.

Insurance Companies: Better Value?

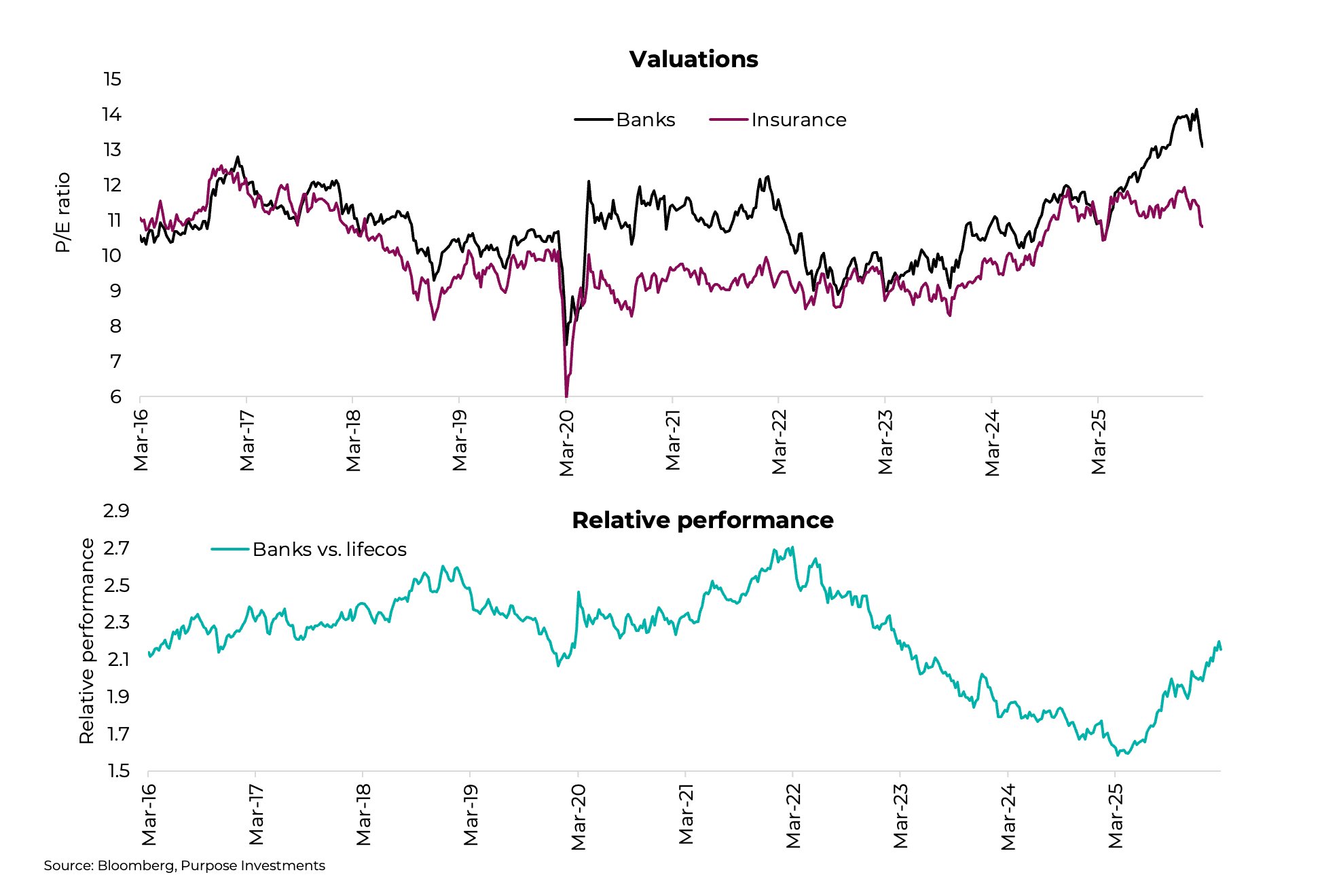

There does appear to be better value elsewhere in the Canadian Financials sector. For the TSX, Financials carry a 31% weight: 21% is banks, and the remainder is split between insurance and capital markets. Of interest is the valuation spread between banks and insurance.

The stronger relative performance of the banks compared to the insurance sub-indices for the TSX has led to a rather high historical valuation gap. Insurance companies may not be cheap on an absolute basis, but they certainly offer better value relative to banks, and many of the underlying insurance companies have similar growth profiles.

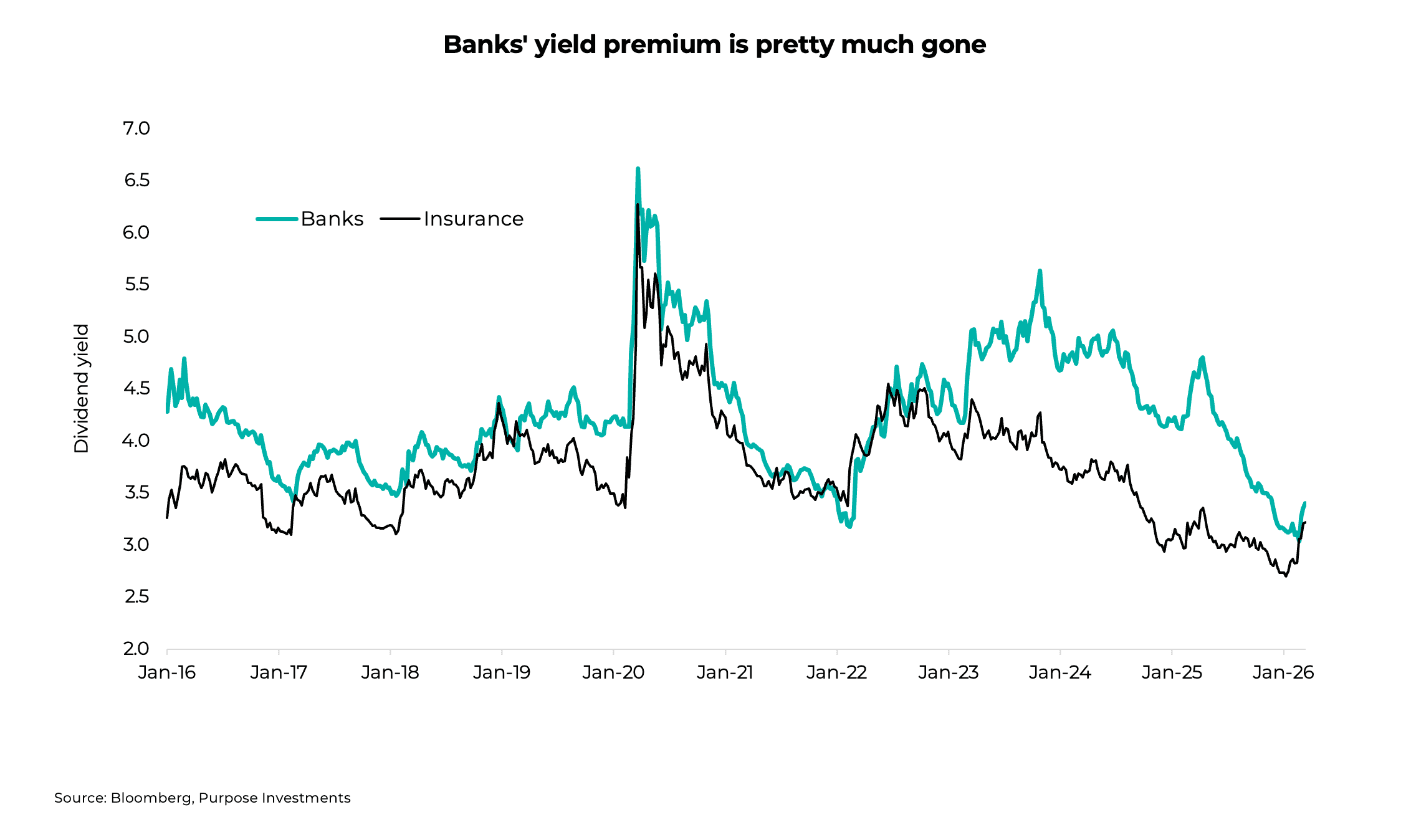

For those lovers of dividends — hopefully all of us, because we are Canadian after all — the higher dividend yield offered from banks appears to have almost disappeared relative to insurance.

Final Thoughts

Obviously, Canadian portfolios pretty much always have some exposure to banks; they’re simply such a big part of our market. The dividends are also an attractive attribute. Plus, the insurance space has historically been a bit higher beta. But given valuations, growth and current dividend yields, we’re a bit more positive on insurance and a bit more cautious on the banks.

— Craig Basinger is the Chief Market Strategist at Purpose Investments

Get the latest market insights in your inbox every week.

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.