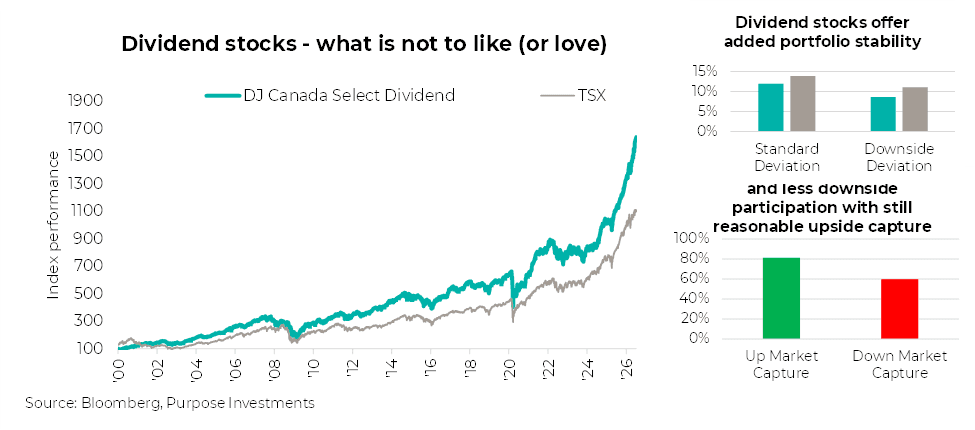

Canadians have unconditional love for dividends for good reason. One reason is the bad historical experience in most other parts of the Canadian equity market. Whether it was technology, health care, fertilizers, marijuana, gold, base metals, forestry, energy, all had some great runs but then ended poorly. Meanwhile the Canadian dividend tilted strategies kept steadily marching higher. Add some decent tax treatment for Canadian dividends, it’s a bonus.

Past performance speaks volumes to how Canadian dividend investors have been rewarded. Stronger performance than the broader market, less volatility measured by either standard deviation or downside deviation, reasonable upmarket capture and significantly less down-market capture. It gets even better as dividend growth in Canada has dramatically outpaced inflation. Even over the past 5-year period, with inflation rising about 20% dividends for the TSX Composite grew by 44% and even higher for the DJ Canada Select Dividend index.

One secular factor that helped provide a tailwind for dividend stocks over previous decades was low and falling bond yields. As bond yields fell in the 2000-2020, investors went looking elsewhere for income, and dividend stocks were a popular destination. This contributed not just to performance but also lower risk metrics. Consistent inflows will do that.

But in 2021, bond yields headed back up and have remained at higher levels for years now. Clearly the falling yield tailwind is gone. In fact, over the past five years, the performance between the DJ Canada Select Dividend index and the TSX Composite are roughly equal (+15% annualized). Also of note, the volatility is also about equal. Standard deviation since the start of 2021 is 12% for both indices and downside deviation is a tie at 6%. So, in a higher or more normal yield environment, perhaps the defensiveness of the dividend factor doesn’t hold. Fortunately, with performance annualizing at 15%, clearly nobody seems to mind.

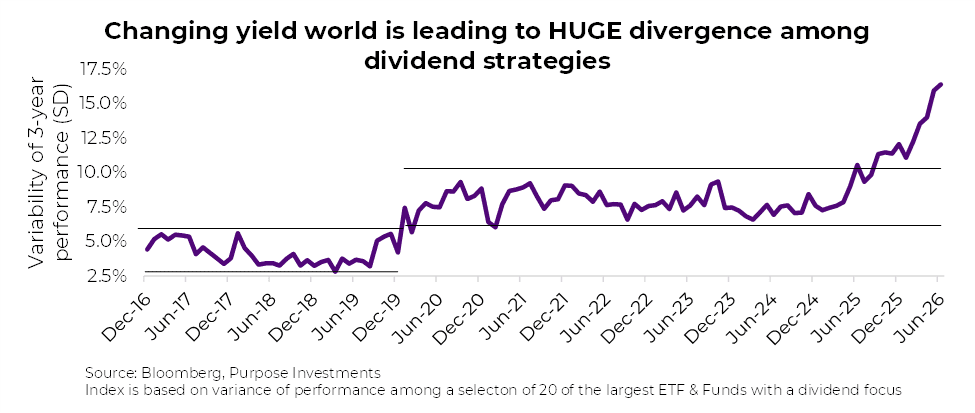

One area that is more interesting and impactful on how you get dividend exposure is the divergence among strategies. You see, when bond yields were falling, helping lift dividend stocks higher, it didn’t really matter how you chose to get exposure to dividend paying companies. Invest in a basket of dividend stocks directly, use a passive rules-based solution or an active manger, they all kind of performed much the same.

But now, or since bond yields normalized, how you get exposure to dividends really matters. This can be seen in the divergence in performance among dividend strategies. The following chart shows the variation in performance among the largest dividend focused ETFs or Funds in Canada. As bond yields fell in the 2010s, performance dispersion among strategies was very narrow. As yields rose, it widened and more recently widened even more.

Suddenly, it matters how you are getting your dividend exposure. The mega factor of falling yields is now a smaller factor and other factors have become more important. Is the portfolio concentrated or diversified? If concentrated, is it concentrated in the right sectors or the wrong ones? And if in the right ones, will they be the right ones in the next twelve months?

In 2025, having some gold made a big difference. In 2026, energy was the big driver in the early months and now it’s the banks…what is next? The dividend space appears to have become more rotational which does have some important implications. The star of one period, because it has a very high concentration in the right sector or factor, may become the dog in the next period. As of this point in 2026, those dividend ETFs or funds that have 50%+ financials are the stars.

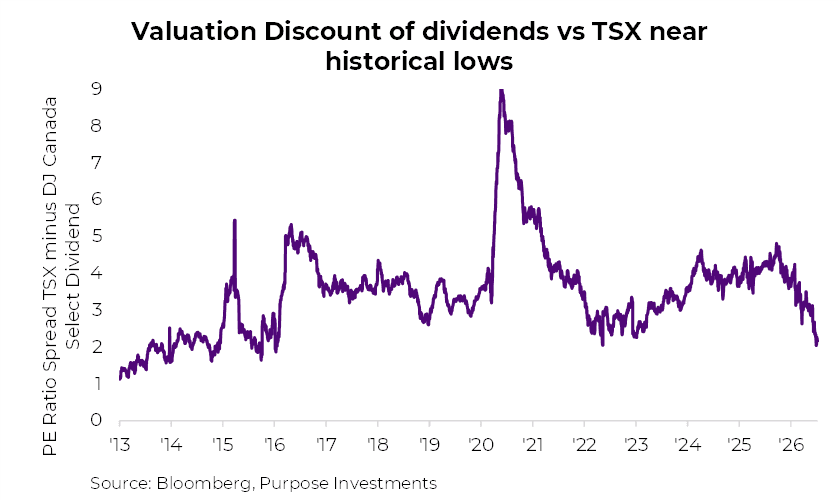

The good news is nobody is unhappy given performance has been strong all around. The challenge going forward may be that even the dividend space is pretty stretched. The broader market, TSX Composite, is down to about 2% yield. The DJ Canada Select Dividend index is yielding more, but it too is near multi-year lows. Turning to valuation, dividend indices have consistently traded at a discount to the broader market. This is because dividend companies tend to be more mature, slower growth businesses, that warrant a more conservative multiple. But today, the spread between the DJ Select Dividend Index and the TSX Composite is at its lowest in many years.

Final Thoughts

Dividend yields are down due to strong price appreciation. This does have dividends relatively more expensive than they have been in a long time. So, what is a dividend investor to do? Check your dividend exposure, even if it is doing really well. It may be just super concentrated in what has worked lately, which makes it extra risky. We do believe with leadership rotating in the dividend space, a more active strategy that can take advantage of opportunities or these rotations should have an advantage. Of course, picking the rotation is the harder part.

Regardless of your chosen approach, with available yields on the lower end due to price appreciation and valuations less appealing, diversification may be even more important going forward. Avoiding strategies that are overly concentrated and opting for better diversification is perhaps more important going forward than it was in years past.

Check how you are getting exposure to the dividend factor.

— Craig Basinger at Purpose Investments.

Get the latest market insights in your inbox every week.

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.