Many things move the share price of a company. There are the big macro factors such as the broader market, big economic data, interest rates and geopolitical factors. Company specific factors as well such as guidance, earnings or specific news. And then there is the story or prevailing narrative in the market. Think of it as what people are saying about a company, industry or asset class. This narrative can be very powerful on share prices.

We believe this in an increasingly narrative driven market. All those other factors still matter and will move prices, but the narrative seems to be carrying a much bigger weight as of late. The allure of a narrative is it explains a very complex situation and boils it down to a short simple story, that sounds smart. And us humans, we like stories as it was part of our evolution. Information has always been passed along better in a story format.

Bitcoin is down over 20% in the past month, with the most prevalent narrative (story) that investors are selling to free up cash to possibly participate in the SpaceX IPO. Plausible? Sure. Provable? Nope. It does take the price of bitcoin, which is influenced by many factors, and explains what is happening with a reason that sounds smart enough. Unfortunately, there are so many moving parts in the market, so many participants, so many different motivations, a simple narrative is a short cut.

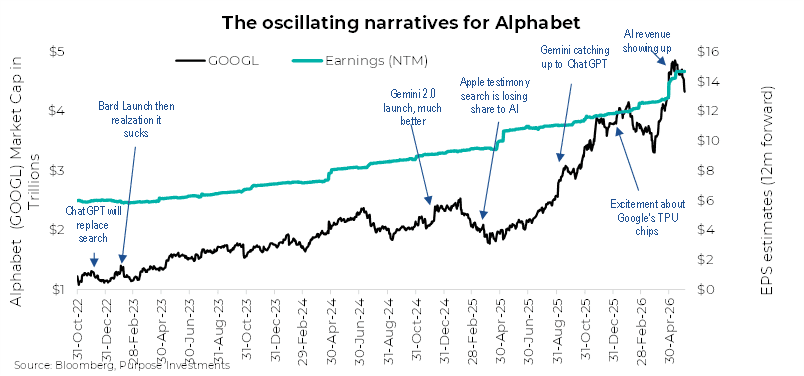

While a story maybe a short cut, that doesn’t mean it doesn’t move markets. And it doesn’t remain constant. Take a look at Alphabet (Google) over the past few years. Very impressive with steady earnings growth from $6 per share to just over $14. Meanwhile, the market cap has grown from a bit over $1 trillion to brush up against $5 trillion over that same time period, and certainly not a smooth line like earnings. When their initial AI tool Bard was launched, the stock went down 20% as it failed to impress. There were also periods when fear AI would cannibalize or replace simple search, weighed on the stock. Given advertising on Google is estimated at 70% of sales, it’s a legit fear. Then with Gemini, AI was incorporated into search, they gained market share and the narrative turned back to being positive. Then TPU excitement, then AI revenue started to show up, almost making it the most valued company in the world.

All these oscillating narratives have some fundamental foundation, but it sure seems the narrative carries a lot of weight. The price-to-earnings ratio of Alphabet ranged from a low of 14x to a high of 28x. In our view, it could be hard to justify these price variances with a discounted cash flow model after feeding it stable earnings growth.

This market has become very narrative driven, with the narratives driving some things up and some things down. And the narratives don’t even have to change; they can simply become less prominent or fade away. Perhaps an over simplified approach to show this is with google trends, measuring key word usage in search queries. It doesn’t capture what the narrative is, positive or negative, but provides a proxy of how loud a narrative has grown.

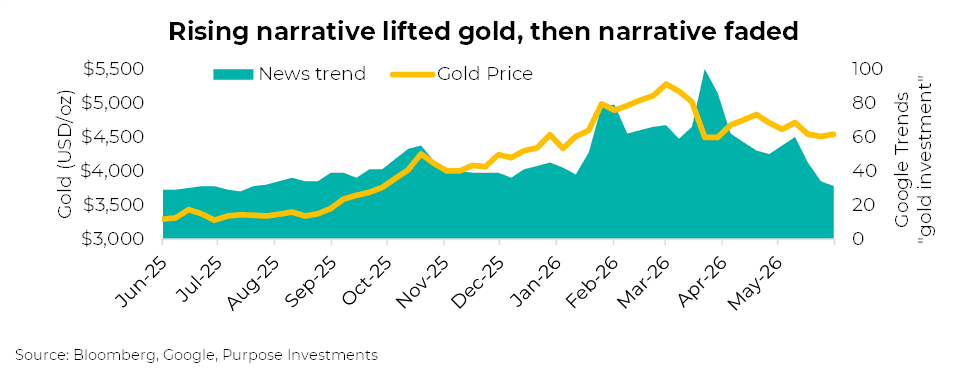

Gold had a pretty epic run in late 2025 into early 2026 and has been languishing over the past few months. Many factors influence the price of gold, but the narrative certainly matters. The first two peaks in Google trends were roughly inline with gold price peaks. The big peak in the narrative flow was after the war started and the price of gold dropped. Very possible the narrative flipped from loving gold to wondering why it isn’t working during war time. Nonetheless, the interest in gold has faded, as has the price. For now, anyhow.

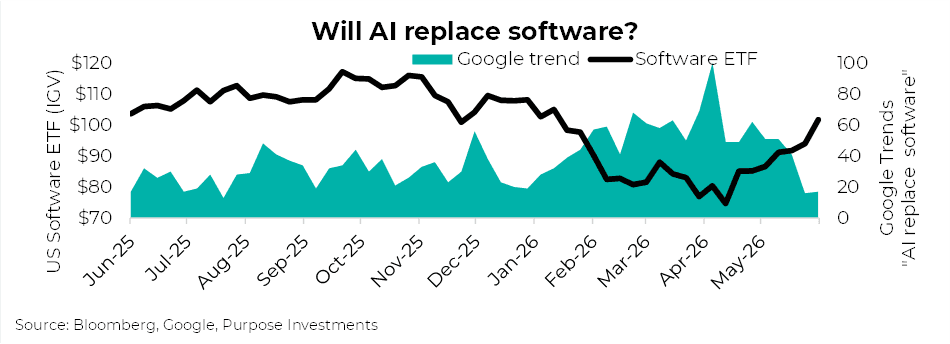

Here is one narrative even more on point. A narrative started to build late last year that AI would kill or really hurt many software companies. The premise was (and is) AI can more quickly or cheaply create software, which would allow a new competitor to come in with solutions at much lower price points. This would put pricing pressure on software companies. This narrative (fearful one) pushed software valuations from over 30x to under 20x in a few months, with share prices falling 25% based on the S&P 500 Software index.

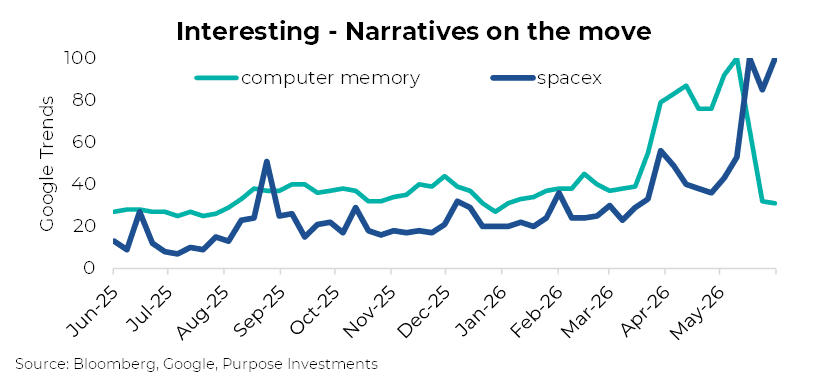

This risk hasn’t disappeared, but the narrative has. And share prices have recouped most of the losses. In our view, markets often appear to overreact in the short-term and under react in the long-term. Narratives drive that short-term over reaction. Here are two big narratives of late, computer memory and SpaceX.

Why is this a narrative driven market?

Full disclosure, in our attempt to answer this question we are going to tell you a story. It is plausible but sadly hard to prove. We believe there are two key factors behind this more narrative driven market dynamic: late cycle & AI.

Late Cycle – We believe it is late cycle because of how long this cycle has run, inflation is pretty hot, output gap is largely closed, commodity prices up, late cyclicals are performing strongly, employment is tight, consumer starting to weaken and of course a big disruptive technology story.

In the late cycle, stories tend to resonate more broadly and carry a bigger weight. The Internet, housing, China, Mag7, AI, these stories captivate and counter arguments are dismissed with “they just don’t get it”. As the cycle ages, strong performance and a fading memory the past bear market cause investors to become more fearless. It is a more fertile environment for stories to resonate.

Artificial Intelligence – This one has a few nuances. Firstly, whenever there is a big disruption, such as AI, the fundamentals become hard to conceptualize and stories fill the void. Maybe not simple valuations like PE, which are a bit stretched but not insane. It could be a size thing. Remember that chart for Alphabet that experienced a 20% drop when they launched Bard? That drop was about $200 billion in market cap. If they fell 20% today, it’s a Trillion dollars of wealth that would disappear.

The dollars being thrown around are pretty insane, not implying they are made up or anything. Just hard to process mentally and stories can help with that.

Secondly, it may be algos. AI has enabled just about anyone to build an algorithm trading strategy. Upload a bunch of data, throw together some well designed prompts and have AI build your strategy. Few more prompts and you can tie it into a trading platform. Ok, it’s not that easy but it is a heck of a lot easier than before AI.

Sure, the quant shops are far superior in design, testing, implementing, monitoring and are regulated. But this DIY approach has likely lowered the barriers of entry. AI has enabled algos to be quickly developed on sentiment, news flow, momentum, etc. There is some indication that AI is more prevalent in the market as trading volumes have declined during periods of key AI platforms outages.

Now if we truly have many DIY algo traders building strategies all based on the same LLMs, well, is it a surprise their signals would cluster together? A narrative could start to build, the algos find it and start trading on it, this fuels the narrative to become more widespread.

How do you invest in a narrative driven market?

This is a challenging question which we will attempt to answer with our three sample investors: Thomas Bayes, John Maynard Keynes and Dug.

Thomas Bayes: Creator of Bayes Theorem, has a view of the world, acknowledges the future is unknowable and uses a weighted probability approach to encapsulate his views. These probabilities are adjusted as new evidence is encountered. Call it a gradual, or fluid approach to changing his views on the world.

John Maynard Keynes: Often referred to as the father of modern economics but is perhaps more known for the quote “When my information changes, I alter my conclusions. What do you do, sir?”. In this case, Keynes doesn’t change his mind until the evidence accumulates enough to warrant the change. Slower to change his mind, but then abrupt and decisive.

Dug: The Golden Retriever from Up was famous for being distracted by squirrels. His famous quote is “My name is Dug. I have just met you, and I love you.” Dug changes his mind quickly and will change it back just as fast.

Given a narrative can drive stocks in one direction for a period and then the narrative moves elsewhere, Keynes probably wouldn’t manage well. Too slow to change his mind and he may just do so near the top (or bottom). Bayes would likely do better, incorporating a new narrative sooner albeit with a lower weighting. And when the narrative changes, would gradually incorporate this as well. Better, but not great.

Dug, clearly the cutest, may have the investment edge here. The ability to change his mind quickly as the narrative oscillates. Unfortunately, from a portfolio perspective changing your mind too quickly can easily lead to over trading and often poor results. Perhaps the overall portfolio should be managed by Bayes with a little Dug allocation on the side.

Momentum can do well when narratives dominate

If building your own algo, trading strategy that digests news from multiple feeds (plus Reddit and Twitter) and synthesizing the flow to create trading signals is something still out of reach, momentum may be the answer. Momentum, which is based on price momentum of the market, sectors or individual equities, captures the narratives as they show up in market prices.

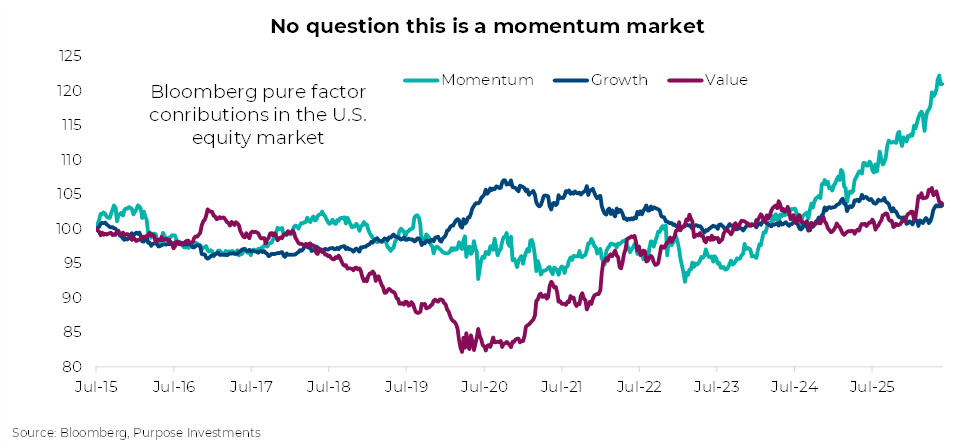

Bloomberg Pure factors break down market performance into many categories. Value and Growth are the most common, but Momentum is getting more attention, helped by its rapid rise as a performance driving factor. Since mid 2023, momentum has become the dominant driver of performance, among other factors.

This is likely more evidence we are in a narrative driven market. It sure isn’t value, quality, or even growth. The challenge would be as the narrative changes, will the momentum index or factor reconstitute itself quickly enough? Nothing is as fast as Dug.

If the narrative driven market continues, momentum is likely a useful factor. But it can also be pretty risky if things reverse. That is certainly evident in the last few days as leadership switched from the high momentum to value/defensive pockets of the market. At the time of writing this (early afternoon of Friday, June 5), the iShares MSCI USA Momentum Factor ETF is down 5% in two days. Still up 24% this year, but clearly if the narrative or market leadership has changed, watchout.

Final Thoughts

This is late cycle and a narrative driven market. We don’t think it ends anytime soon but do expect narratives to drive markets in both directions as the sentiment or excitement oscillates. Late cycle can go on for some time and often see some of the biggest moves. Fundamentals, the economy, rates and other factors will become important again, but in the meantime it’s the stories.

— Craig Basinger & Derek Benedet at Purpose Investments.

Get the latest market insights in your inbox every week.

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.