Most of the U.S. Treasury market conversation right now is about supply. How many bonds and bills are being issued, what duration, whether the deficit trajectory is sustainable. Fair enough, the numbers are mind-blowing with big supply getting bigger. But we think the more interesting question is sitting on the other side of that trade – who is actually buying this stuff? And as the composition of that buyer base changes, how should we think about yield risk? We think it does matter and the shift is bigger than most people realize.

[Note to reader: we are proudly Canadian but given this is focused on U.S. Treasury bonds, this is written from a U.S. perspective until we bring it back to why it matters for us Canadians near the end.]

The Architecture Flipped and Nobody Made a Big Deal About It

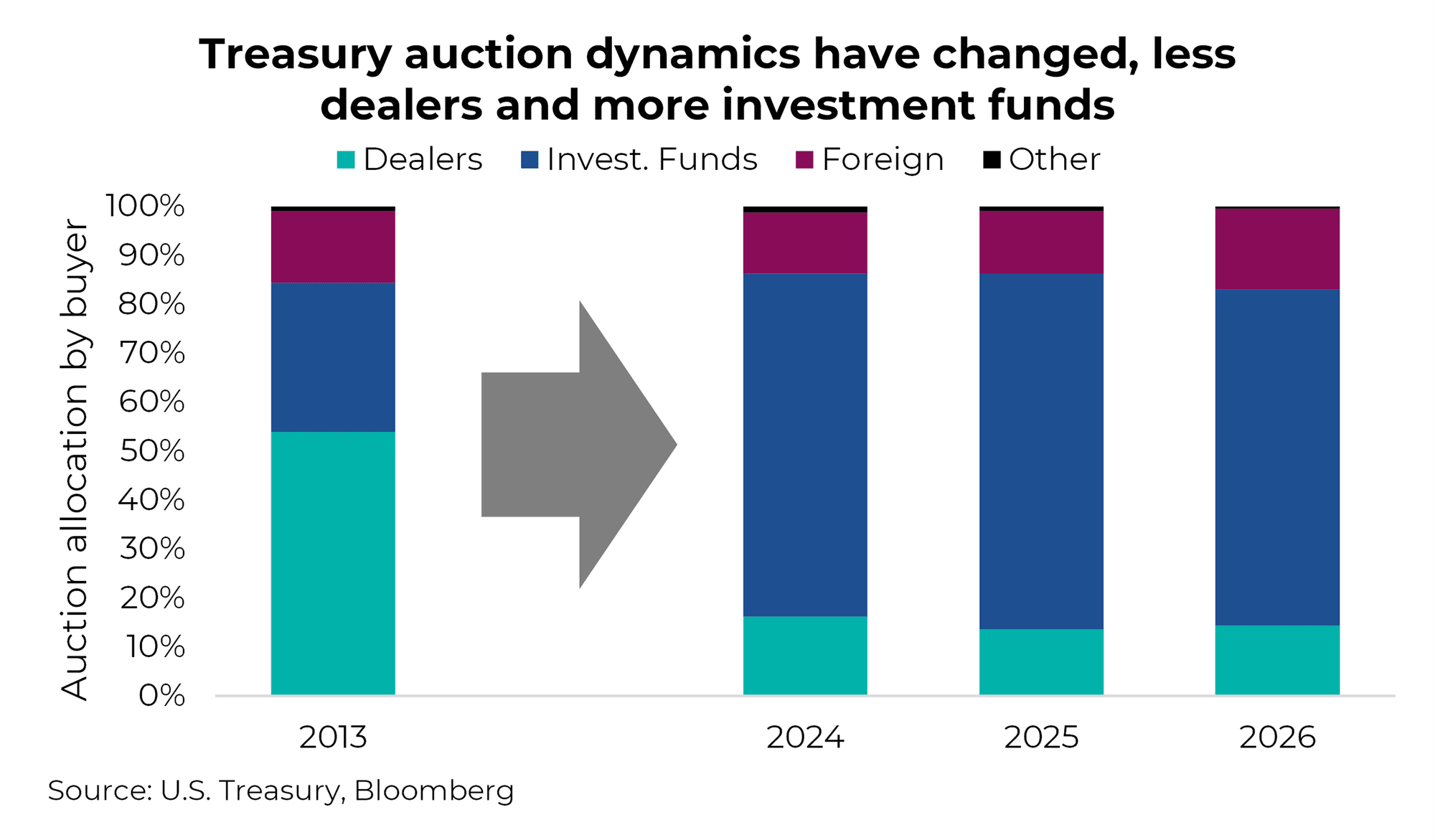

Here is a number that should probably get more airtime than just the size of deficits. In 2013, primary dealers took 54% of all Treasury coupon auctions but so far in 2026, they have taken down just 14%. Domestic investment funds now absorb roughly 70% of issuances, a consistent share for the past three years. With those moody foreign buyers at 16% year-to-date, up a bit from 13% in 2025.

This is not a marginal shift, it is a structural reordering of who buys all these Treasuries. And the “who” matters.

Think of dealers as the old shock absorbers in this market. They absorbed, warehoused it and distributed it over time. Price-insensitive in the short run because they had to be and it was literally their function. That buffer is mostly gone. In its place is a 70% share owned by domestic investment funds that have real opinions about whether the yield is adequate and real options if it isn't. The shock absorber has been replaced by a buyer who has both a view and a choice.

Bond Buyers have Changed and They are Yield Sensitive

There are many buyers of government bonds, ranging from big central banks, pension funds, insurance companies, banks and individual investors. The proportions of these cohorts change over time for many reasons. Today, we believe the groups whose demand is more sensitive to different yields, have a larger representation.

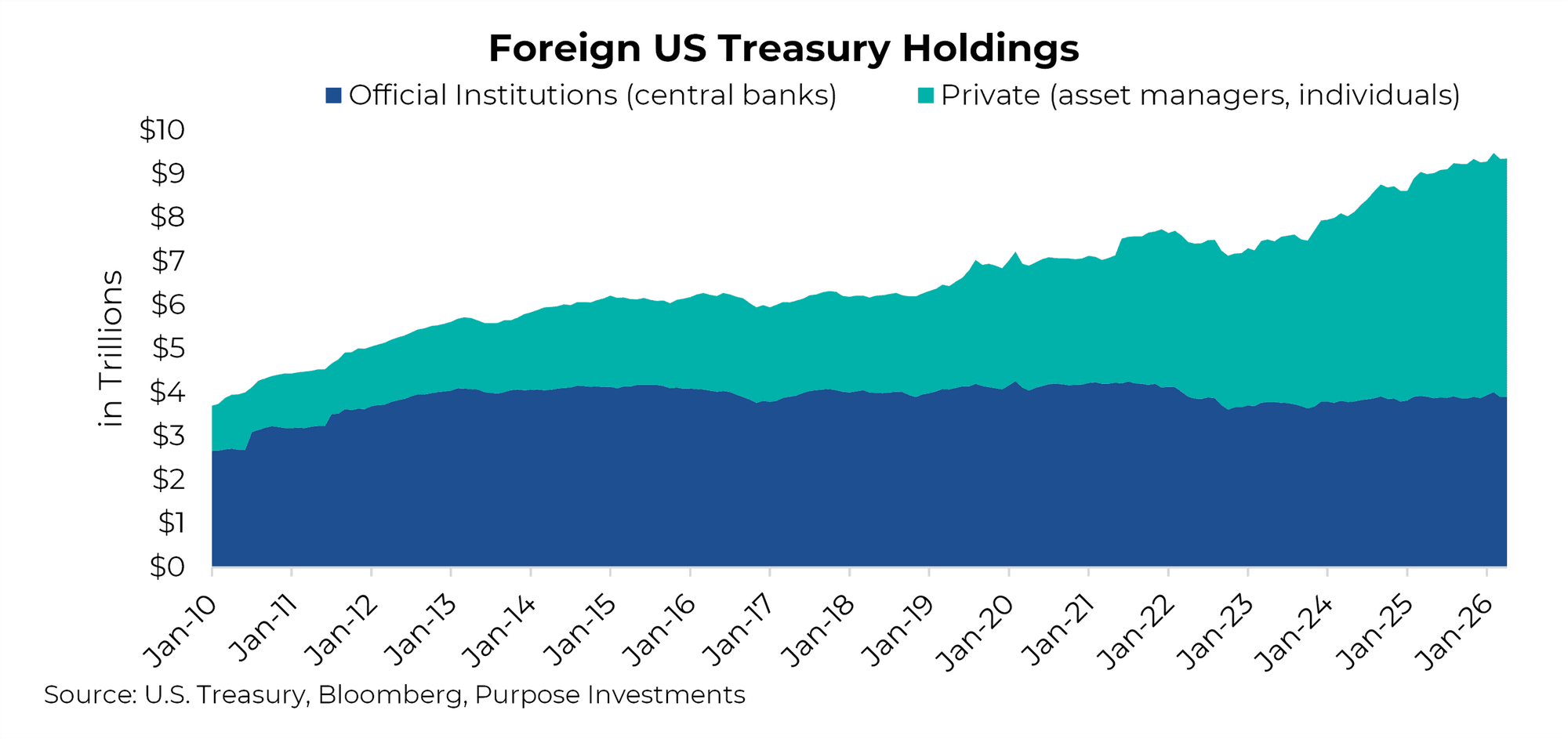

Foreign Buyers - One bond buyer that gets a lot of attention is foreign holders – central banks, sovereign wealth funds that have been steady sellers. For example, China reduced its holdings significantly while Japan stopped adding. But total foreign holdings haven't collapsed and have actually continued to increase. The central bank holdings have flatlined, but private foreign capital replaced the sovereign bid.

Private foreign capital are asset managers or individuals who behave very differently than central bank buyers. Official institutions, such as foreign central banks, tend to buy short-term Treasuries for liquidity management and really don’t care about the yield. Private foreign buyers do care about the yield and often prefer buying duration.

The good news is foreigners are still buying bonds and they are buying longer duration. The bad news is since it comprises of more private foreign capital, they care about yield, so if a yield isn’t high enough they are less interested. They are more yield sensitive.

Annual net foreign private transactions in US bonds and notes have averaged over $500 billion per year since 2022. These are bonds, not just short-term T-bills. They are buying duration and at scale. What triggered this cohort to become meaningful buyers of Treasuries – higher yields. Though full disclosure – the 2026 pace is moderating, and we are watching that closely.

Structural Buyers – There is a large and growing pool of money that structurally needs to own bonds such as pension funds, life insurance, P&C insurance, basically any provider that has to manage a portfolio against long-duration liabilities. While this cohort is somewhat of a forced buyer, they appear to be sensitive to yield and credit spreads.

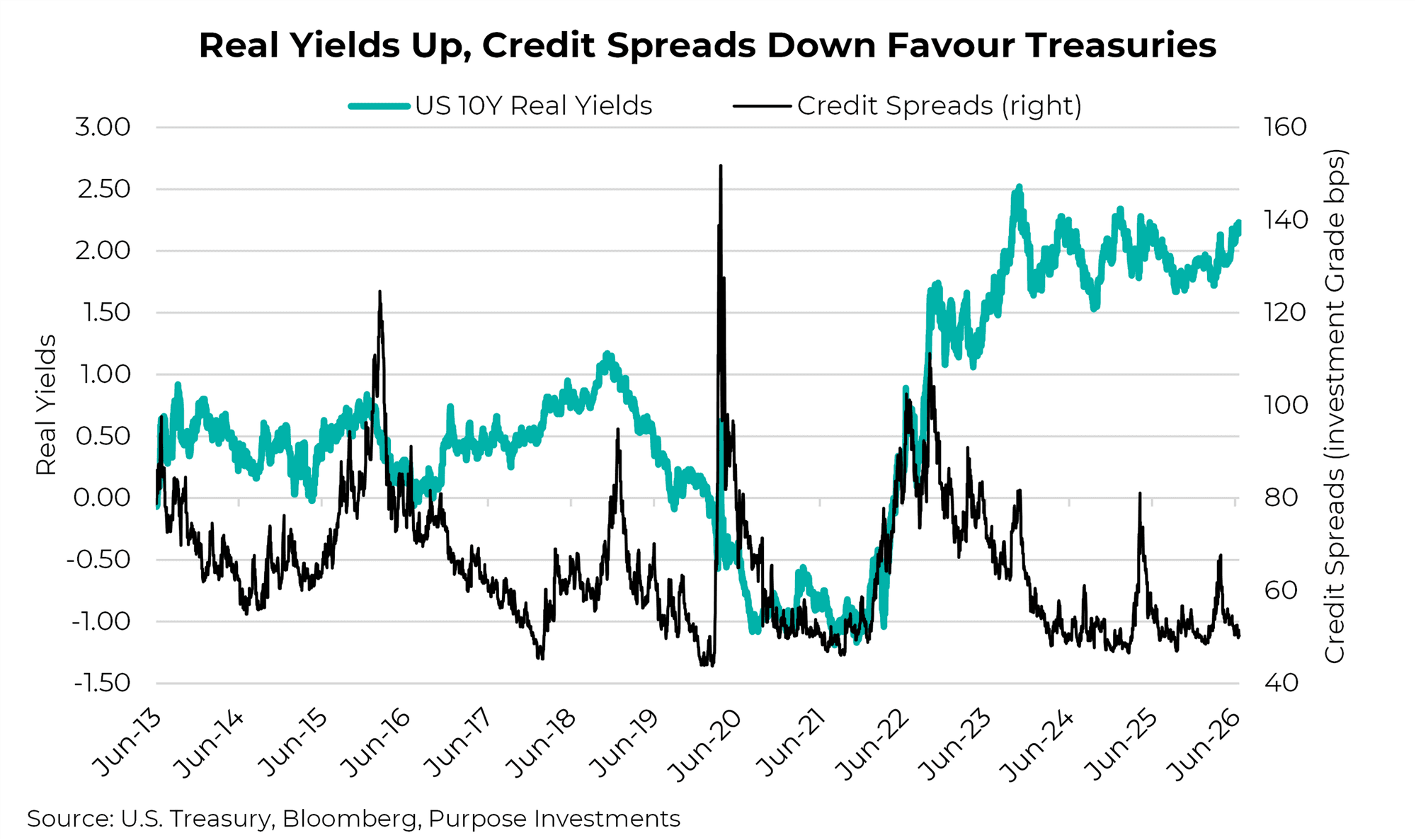

For years the math didn't work. The 10-year real yield spent most of 2012 to 2022 below 1%, with extended periods below zero (real yield is nominal less inflation). As a result these buyers went elsewhere - corporate bonds, private credit, anything paying a real return. That wasn't irrationality, it was math required to offset future liabilities.

The math has changed as the 10-year real yield is now 2.17%, as of June 22nd 2026, the highest sustained level since before the Global Financial Crisis. Meanwhile credit spreads are near their tightest since September 2011. Thin credit spreads and real yields that are reasonable, the relative value argument for Treasuries over corporates essentially makes itself. You don't need a strong view on duration to own the bond, you just need to be able to read a spreadsheet.

The specific level the research identifies is 5.1% on the 30-year. Above that, liability-driven investors incrementally buy Treasuries to cover new liabilities rather than chasing spread product (credit). We want to be careful not to treat this as a hard floor - it's more of a gravitational pull. But we are close to it right now, and the direction of travel matters.

The Last Auction – The June 11 30-year auction said something plainly. The $22 billion offering tailed by 1.2 basis points – it cleared at a higher yield than where the market was trading beforehand. Buyers required a concession to show up. End-user takedown was 85%, below the recent average of 90%. Indirect bidders took 60% versus their average of 66%. Primary dealers absorbed 15% versus their average of 10%. Dealers are the buyer of last resort. When real money steps back, dealers catch the residual. That is what happened here. The market cleared but it needed to be paid more than expected to do so.

One auction is not a trend. But it is consistent with everything else we've described – a buyer base that is real and structural and capable, but price-sensitive (or yield sensitive) in a way the old architecture simply was not.

Elasticity of Yield Demand

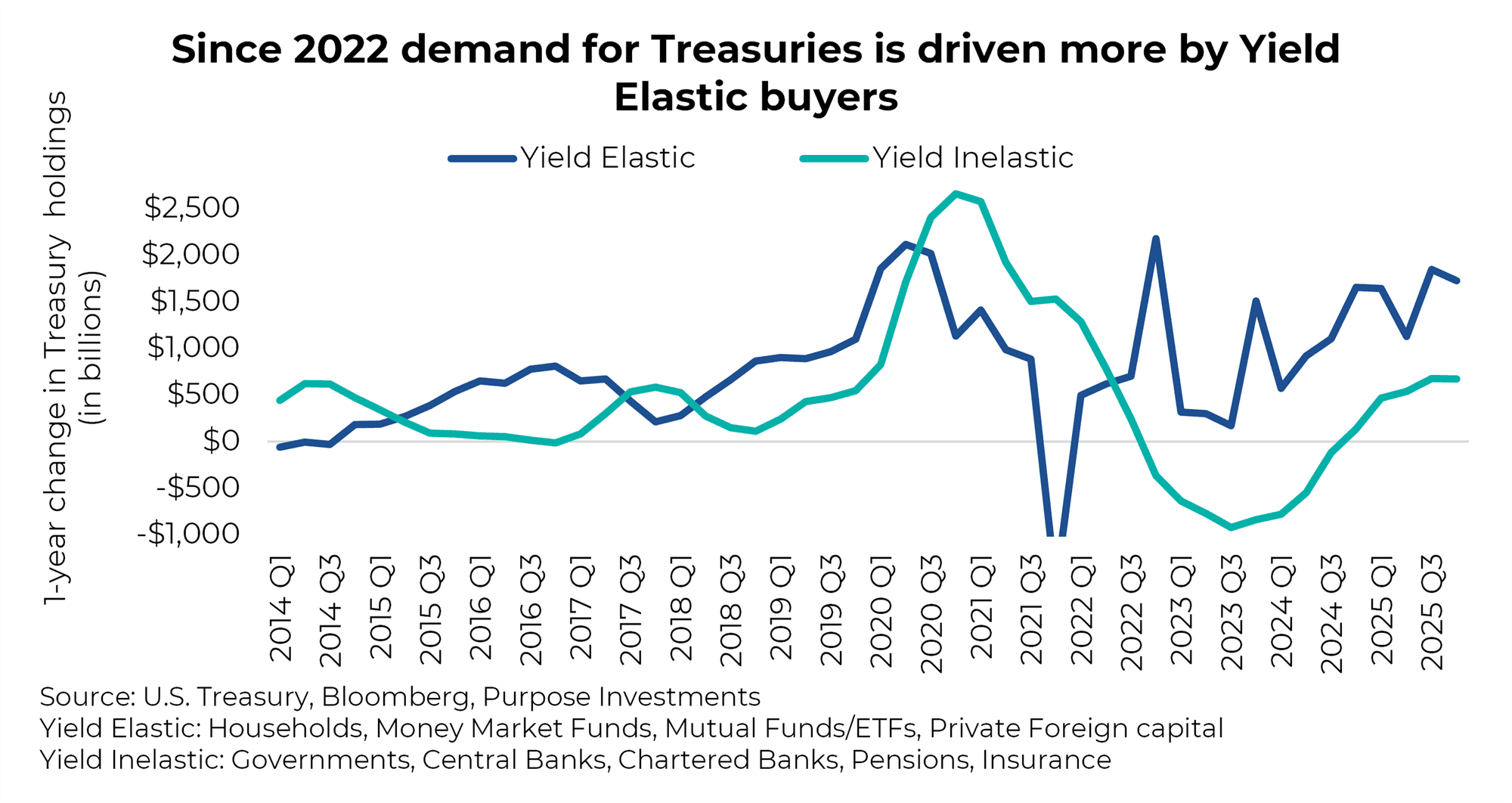

Add it all up, more and more of the demand for Treasury bonds is comprised of participants that care more about the level of yield (yield elastic buyers). Long gone are the days that buyers show up regardless of the yield available for U.S. government bonds (yield inelastic buyers). Note that yield inelastic buyer demand tends to be smoother and yield elastic buyers tend to be more erratic (next chart), depending on many factors but most impactful is likely the prevailing yield. The bad news is this could keep yields higher, to garner enough demand. The good news is if yields rise, it is met with more enthusiastic buyers. Conversely, if yields fall the demand diminishes. In our view, yields could remain higher but also somewhat rangebound.

Bringing it in for Canadian Investors

Like it or not, bond yields globally tend to be impacted by U.S. Treasury yields, so this matters regardless of where your bond allocations are domiciled. In our view, we are in an era of higher yields and given the elasticity of demand, this could stay. The good news is those higher yields now carry a real yield in government bonds that is reasonable, perhaps even attractive given the low incremental spread pickup available by moving down the credit spectrum.

What makes the setup interesting to us is that the structural demand story may soon shift from a headwind to a potential tailwind. Research suggests that the yield levels required to attract more pension funds, insurers, and liability-driven investors back into the Treasury market are not far from where we are today. This could help provide a ceiling should yields move up.

We are not dismissing the supply concerns or unsettling fiscal trajectory. But the demand pool could be deeper than the supply narrative implies and we know roughly who the buyers are, what they currently own instead, and at what yield level the math starts working for them. Sticky sovereign capital has been replaced by yield-sensitive private capital - more duration-tolerant than what it replaced, but also more straightforward about what it needs to show up – an attractive yield. That is not a bad thing – it is actually exactly how this is supposed to work.

-- Hilbert Wan at Purpose Investments.

Get the latest market insights in your inbox every week.

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.