"It never was my thinking that made the big money for me. It always was my sitting.” – Jesse Livermore from Reminiscences of a Stock Operator (1923)

We curated the title of this Market Ethos from Reminiscences of a Stock Operator, a timely classic about the life of Jesse Livermore. He earned the nickname “Boy Plunger” for taking large speculative bets, including profiting massively during the crashes of 1907 and 1929. Going long or short in stocks and commodities, you might think this has nothing to do with investing today or your portfolio, but there are valuable lessons for every investor from his journey. Specifically, his acknowledgment that his profits didn’t really come from making awesome well-timed trades ahead of the market’s next gyration, his profits came from the sitting.

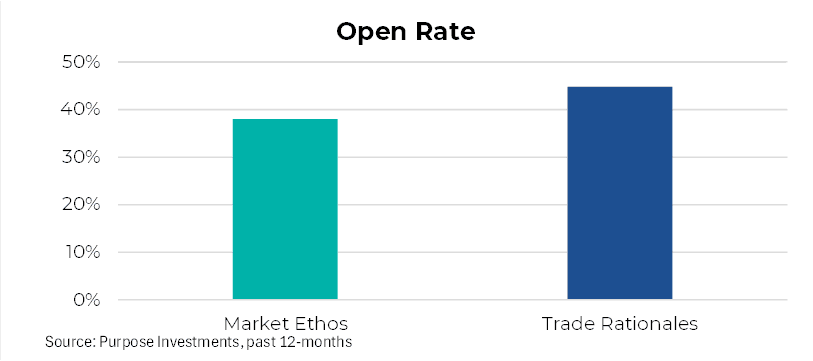

Fast forward a century or so to current times, things have not changed that much. Headlines or attention is primarily focused on the transaction. What did a famous portfolio manager buy or sell garners most of the markets or media’s attention. There are even funds and ETFs that copy famous hedge fund managers’ trades once made public in filings. This attention on the trade is not lost on us, based on readership of our content. Not implying we are famous but trade rationales we circulate after making changes in Purpose Investment’s multi-asset portfolios have some of the highest open/click rates among our many publications (even higher than Market Ethos if you can imagine).

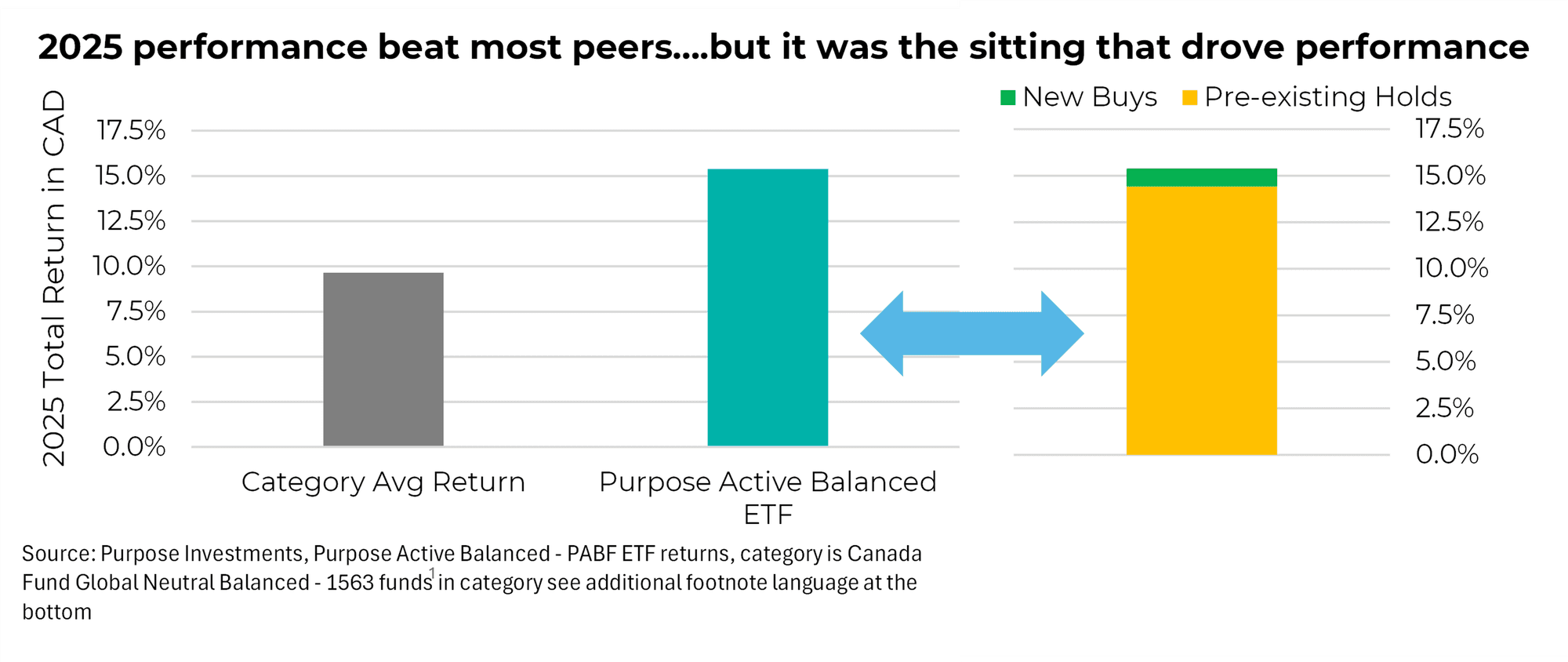

But guess what, it is the pre-existing holdings that often drive the performance over a given period. For illustrative purposes, Purpose Investments took their multi-asset strategy and broke down the performance contribution into pre-existing holds and new buys during 2025. The new buys occurred in the current calendar year while the holds may date back years. About 1% of performance came from the six purchases made during the year, which is only about 6% of the overall return. Our profiting clearly came from sitting on older vintage positions.

So, why is there such a high level of attention via the media, research reports, clicks or questions? “What have you been buying?” is a common one, while research that is an upgrade or downgrade certainly gets read more than an ordinary research update. This attention does appear logical from a behavioural perspective. Investing is dealing with a high degree of uncertainty, and nobody likes uncertainty. Hearing that some “expert” who may be more experienced, have greater insights, or puts more work in has made a transaction piques your interest. And if it aligns with your positioning, it reinforces your thinking.

Plus, everyone seems to adore the “hero” call. That investor or portfolio manager that exited at the top or bought at the bottom. If it is a big enough turn in the market, the subsequent asset inflows really ramp, or the option to go on the speaking tour or write a book. Rockstar award! But investing is the combination of insight and luck when it comes to great timely “calls”. Nobody knows it is the bottom or top.

Context Matters

Investors often look at transactions or trades as insight to where an “expert” believes the market is going. That may be the case in some circumstances, but very often it isn’t. It could be an overall portfolio decision, not necessarily a directional bet. Purpose Investments trimmed gold bullion in April 2025, when gold was fetching a mere $3,300 an ounce. Today, gold is much higher. This decision was driven more by having a good amount of gold years ago that grew into an oversized position last April (a good problem to have), not necessarily a negative view on the near-term path for gold. Similarly, buying into the growth factor was enabled by low overall exposure to it.

Tilts or Exposures Matter More Than Individual Trades

For most portfolios (those that don’t necessarily make big swings), it is the overall exposure that matters more than a specific trade. Sure, a trade can be adding or subtracting from these exposures or tilts, but they are often incremental. If you want to glean insights from other portfolio managers, focus on the whole portfolio and its tilts, not just the transactions at any point in time.

We are not saying trades or transactions don’t matter – the overall portfolio composition is the result of past trades, some recent, some from years ago, or even decades back. Importantly, don’t view trades in isolation. To better understand a trade, it is best to understand the trade in the context of the overall portfolio. Rebalancing, taking some profits, right sizing trades are driven more by portfolio considerations than explicit views on the markets next move. Taking advantage of potentially mispriced assets, those are trades worth more attention.

To finish on a positive, our few trades the trades in the Purpose Investments portfolios in 2026 have contributed more to performance at about 15% of gains. But still, most of the portfolio’s gains in 2026 are coming from sitting on positions, some that have been owned since inception. Patience is a very valuable attribute for successful investing.

— Craig Basinger at Purpose Investments.

Get the latest market insights in your inbox every week.

1. Morningstar Research. The Canadian Investment Funds Standard Committee’s (CIFSC) Global Neutral Balanced category is comprised of funds that invest a minimum of 40% and maximum of 60% of their total assets in equity securities and invest less than 70% of total assets in a combination of Canadian-domiciled equity and Canadian dollar-denominated fixed income securities. Category average performance calculated daily by Morningstar, which constitutes the category monthly by equally weighting all funds, and for each fund equally weighting all the different fee series offered by that fund, in the category. The category average excludes funds that are not priced daily. For more information, click here for the Morningstar category average methodology.

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated. The indicated rate of return is the historical annual compounded total return including changes in share/unit value and reinvestment of all distributions and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any securityholder that would have reduced returns.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.