There's been quite a number of changes to the portfolio over the past couple weeks as we enter the second phase of the Iran / U.S. / Israel conflict. As the probability of kinetic escalation gets priced out of the energy complex, the market has shifted its concerns to the direction of interest rates following a hawkish tone from the new Fed chair Kevin Warsh last week. While volatility remains elevated across many commodities, we remain nimble and focus our efforts on finding companies that can execute regardless of the volatility through the cycle as the whipsaw in headlines continue. With many key resource sectors having come off substantially, we think the real opportunity continues to be ahead of us with much of the "fast money" having left the space in the recent selloff. Below are our key thoughts on the major buckets of the portfolio today:

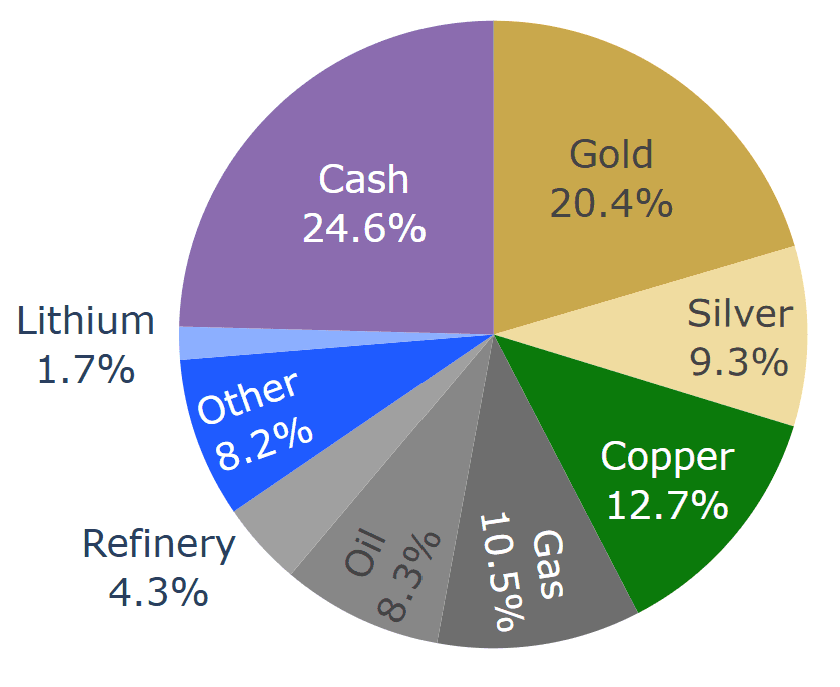

Portfolio weight as of June 26, 2026

Cash

Not a huge topic of discussion historically but our cash weighting has been higher on average over the past 3 months versus historical means of the fund, and we're sitting close to a quarter in the cash today. We have utilized this asset class effectively to minimize drawdowns, and sitting on plenty of cash means a sea of red on the screen does not cost us any sleep. A smart investor once said holding cash is like owning a buy ticket with no expiry date, and the strike price is whatever panic hands you. With 75% of the portfolio still invested we are still very much "in the game", we just lean in when valuations get cheap and lighten up when they run hot. The real payoff comes when the next shock arrives and the crowd freezes, because that is when a buyer with capital can earn several times their money near the lows.

Precious Metals

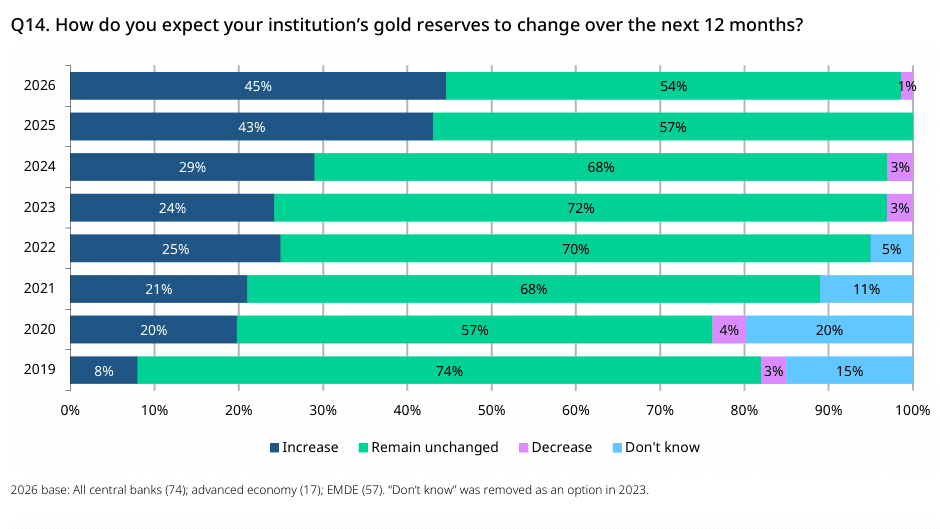

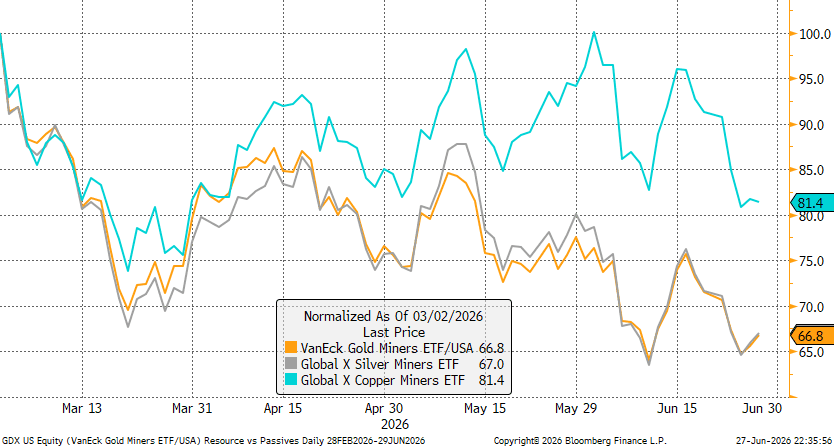

The precious metals have taken a hit on the chin after Warsh's message on prioritizing inflation control during the last FOMC meeting. The USD has been strong since then and precious metals have been inversely correlated since. With GDX/SIL down 33% since the end of February peak, we're ok scaling back into the trade with the move looks overdone. Without going full economist, the market may have over-indexed Warsh's hawkish tone where we think it's a tactic to gain creditability in the market on inflation, and with oil hitting $100+ at one point with Strait of Hormuz still in flux, it would certainly look bad if you're lowering rates going into periods of elevated inflation. Looking at Warsh's track record, he seems to lean hawkish during a Democratic presidency and vice versa for a Republican presidency. He was highly outspoken during the Bernanke QE days where he believed inflation was going to go up substantially and he could not have been more wrong which in itself is fine everyone gets it wrong sometimes, but there hasn't been any real explanation from Warsh on why the world unfolded differently i.e. bank reserves does not equal free money in the chequing account. On the U.S. fiscal deficit story, the two elephants in the room are still healthcare and defense which are both highly sticky spending, the only real lever left that can move the needle and at Warsh's control is interest expense, so we wouldn't be surprised if we see some version of yield curve control come the back half of Q4 to lower this expense i.e. more USD sloshing around backstopping certain part of the curve means a weakening dollar. There's only so many people you can fire from the Department of Education or National Park Service and still wouldn't move the needle and a classic example of penny wise pound foolish. Separately, World Gold Council recently published a survey of reserve managers of central banks around the world and the expectation for central banks to continue increasing gold reserve remains high over the next 12 months. With diesel prices coming down, we also see the mining space back on track from a margin perspective. We have rotated back into mining names where we initially reduced during the opening acts of the war given the expectation of margin compression due to higher energy prices.

Source: World Gold Council

Source: Treasury.gov

Energy

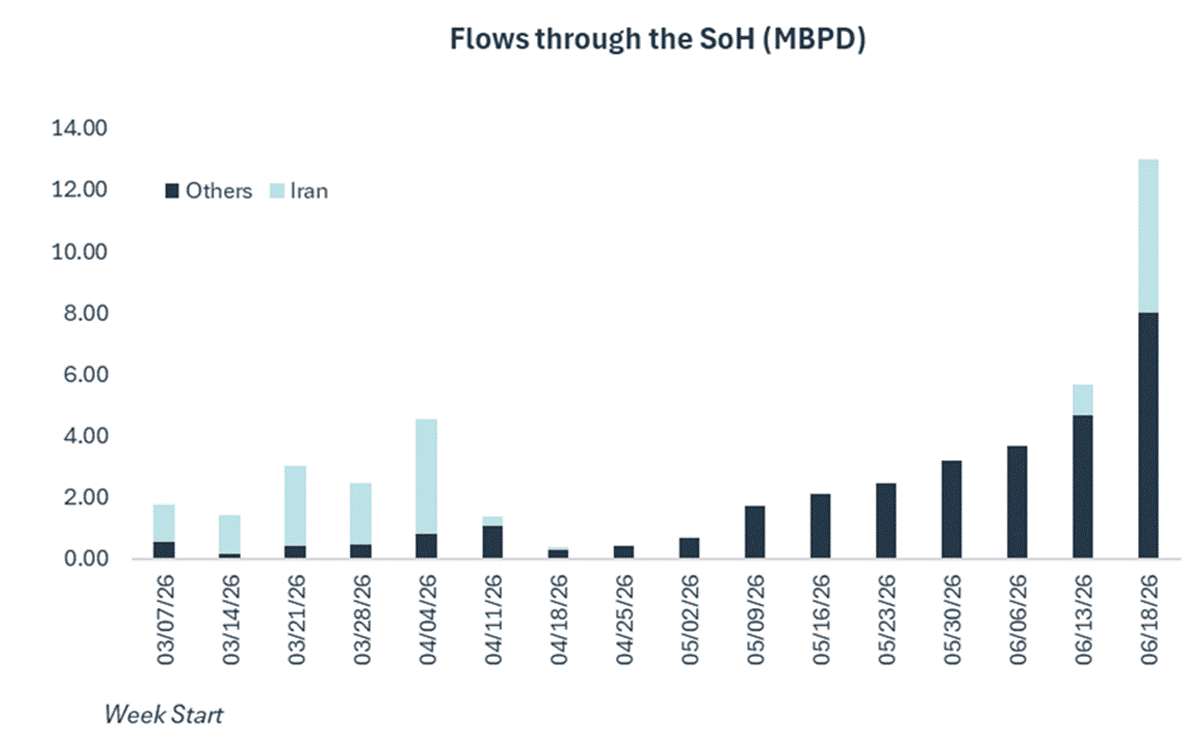

The negotiations are ongoing and will likely going to continue its back and forth state for extended periods of time until the involved parties (including the GCC) can get Israel to back down which at this point is still very much an uncertainty. As of the time of this writing we are still seeing tankers getting attacked and Iranian radar / missile sites getting bombed, so we are still ways away from real "peace".

With the terms that are on the table right now, it seems like Iran has gotten a lot more concessions from the U.S. than the other way around so I don’t see them overplaying their hand at this point, and will likely keep skirmishes going on at the margin to remind the world that they still have the cards, while the U.S. will reciprocate and continue the narrative that they are "keeping Iran in check". We can see that we have reached phase two of the conflict with physical liquids substantially moving out of the Strait of Hormuz and we have also seen evidence of tankers going back in which are initial conditions required for a path of full opening. From a portfolio perspective, we have begun reducing higher oil beta exposure names before version 1 of the MOU came out as we saw rising barrel counts out of the Strait and more importantly tankers starting to feel comfortable getting back in. As of June 18th, we saw a substantial bump of flows through the Strait with Iranian tankers leaving their AIS transponder on and substantial number of tankers taking the opportunity to make their exit which gets us closer (but not yet) to an oversupplied crude picture before the conflict started.

For our remaining energy positions, the top 2 names in our portfolio (Tenaz / Valeura) continue to have world class management team that's executing regardless of where we're at in the cycle, and their niche-y business model lets them have a unique competitive advantage versus others in their peer group. Ironically both names are highly acquisitions driven where M&A has been a huge driver of valuation historically, so lower price decks is when they are able to buy highly accretive deals for the long term. The remaining names we have in the energy allocation of the portfolio remain highly esoteric where today's oil price has very little impact to the upside / downside setup for the companies.

Source: Capital One

Copper

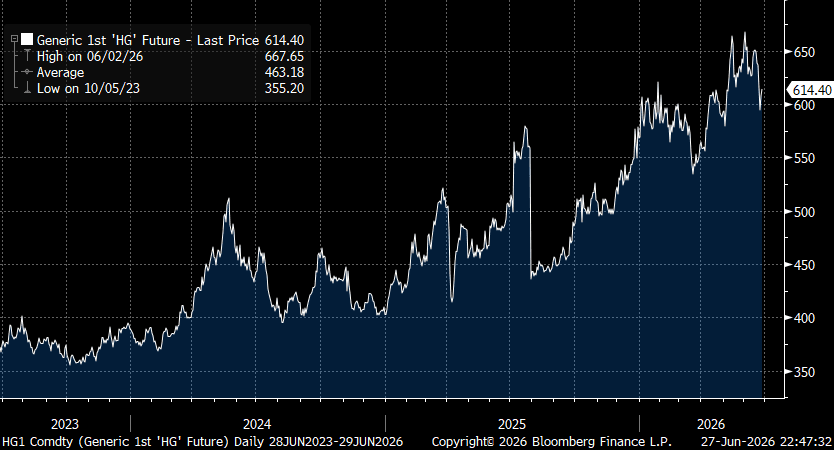

Probably the sector that we're most comfortable sitting on our hands. Copper equities drawdowns versus gold and silver equities have been nowhere as extreme, and also reflective of a less volatile underlying copper prices. The world is short copper today with significant producer outages and we have not made any major copper discoveries for almost a decade. With the AI trade continuing to power forward, a lot of copper is going to be needed for the data center and grid buildout globally.

Source: Bloomberg

Copper prices, Source: Bloomberg

— Ritu Ghai is Senior Director, Product Optimization at Purpose Investments.

The content of this document is for informational purposes only and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document, and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable; however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed; their values change frequently, and past performance may not be repeated.

Certain statements in this document are forward-looking. Forward-looking statements (“FLS”) are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as “may,” “will,” “should,” “could,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions, or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are, by their nature, based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on them. Unless required by applicable law, it is not undertaken, and is specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events, or otherwise.