In the world of asset management, most portfolios are built in isolation. Sharing of ideas is minimal, as anyone you would share something with might be seen as your competition in the industry. It is not necessarily a flaw, it is simply the nature of a business where differentiation matters and processes are closely guarded. The challenge is that it limits perspective. We think there is value in changing that, and in opening the door to a broader view.

Portfolio reviews are one of those things that everyone agrees are important, but the execution often falls short of what they are meant to achieve. In many cases, a review can become simply a confirmation exercise. Typically, much of the focus consists of back tested performance data, some allocation data, and ensuring everything aligns with how you are thinking about the world. There is comfort in that process, certainly when markets have been supportive, and the structure has not been challenged.

This framework is not without its flaws, though. To truly understand the portfolio, you need to go deep. The caveat is that likely reinforces your current view, but does not necessarily test it. A third-party view can bridge that gap, especially as the layers and strategies used in the portfolio become more complex. The data element is crucial, and most data providers will lack in one area or another. This results in an inaccurate look through to the analysis and affects the portfolio decision-making process immensely. For example, one of the most common miscalculations we see is portfolio duration, not because the math is wrong, but because the data point is missing. Forcing you to make a portfolio decision with incomplete information. Knowing what you own is still the right principle, but it requires a deeper level of analysis to actually apply it.

Benefits of looking outside your own portfolio

One of the more interesting benefits of reviewing portfolios at scale is not necessarily identifying what is ‘right’ or ‘wrong’ (a question we get asked a lot), but simply the ability to see what others are doing. Within our framework, we aggregate the data across roughly 60 advisor teams. It is not a massive sample size, but it is a meaningful one. The group is spread across Canada, from bank-owned platforms to independents, and largely consists of high-net-worth focused managers. That gives us a unique lens into how portfolios are built in practice, and you gain that insight through our process.

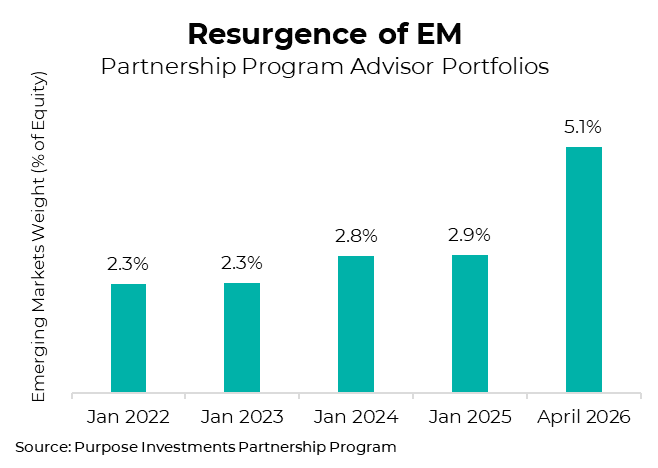

When you look at a single portfolio in isolation, everything tends to make sense because it is your portfolio, and you have a rationale behind it. When you look across 60 portfolios consistently, patterns begin to emerge, and our goal is to share those insights with you in a review. The chart below is a good example of that.

Over the last few years, the average allocation to emerging markets across advisor portfolios in our program has steadily increased, with a fairly significant jump recently. It is not dramatic, but it is consistent and can perhaps provide a bit of confidence with an EM allocation, an area that still has a bit of hesitancy around it for some investors.

This is not about making a call about whether this will be the right decision. Only time will be able to tell that. What it does show is where capital is being allocated and reflects a shift in thinking. At the very least, it might get you thinking about an allocation that is traditionally under-represented in portfolios. These types of insights are very difficult to pick up from your own portfolio alone but become much clearer when viewed in a group.

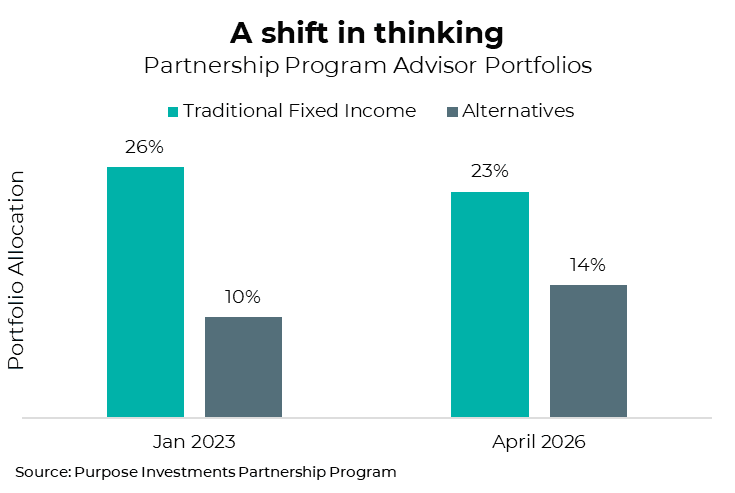

Another trend we have seen in the past couple of years is the shift within the defensive side of the portfolio. The past few corrections have left a bad taste in some portfolio mouths when it comes to bonds. This is apparent when looking at the shift from traditional fixed income to alternatives. Over the last 3 years, average bond exposure has come down while most of that capital has been used to increase the average alt exposure.

Again, this is not a ‘right’ or ‘wrong’ metric, but a data point to view where you land on this spectrum. It highlights how portfolios are evolving, and it can be a shocking number to some people when they see how much the shift has gradually happened in their own portfolio. Will this shift remain long-term, or will we have a true recession where bonds outperform once again, and see allocations revert back to traditional exposures?

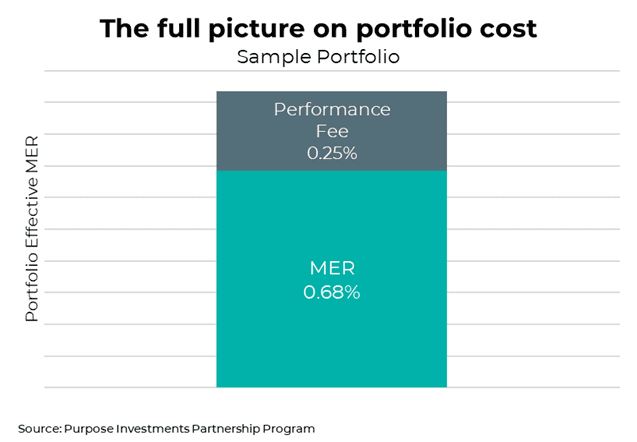

Cost is another area where a more complete view can lead to some interesting conversations. On the surface, most managers have a reasonable understanding of their management expense ratios. Where things become less clear is when performance fees are introduced, particularly if there is a high exposure to liquid alternatives. These are not always the easiest metrics to surface, and as a result, the total cost of the portfolio has actually been higher than believed.

Below is a sample portfolio of a team that we consistently review. The MER without performance fee is just below 70 bps, but when you consider the trailing 12-month performance fee, you get a much stronger representation of what the portfolio has actually cost. For some, this is not a surprise. For others, it can be an eye-opening part of the review and lead to questions about that product.

The Data Problem

All of these insights rely on one key input: accurate underlying data. This is an area often overlooked. Many portfolio analysis tools present information very well, but the underlying data is not always complete. Missing data points, incorrect classifications or partial look-through all have a meaningful impact on the result and the decisions that follow.

We see this most commonly in areas like duration, cost, asset allocation, or even geographic breakdowns. It takes a bit of extra effort to present an accurate look-through of a portfolio, and cleaning the data can be tedious. But this is one of the areas in which we set ourselves apart from peers in the portfolio analysis game. We believe the juice is worth the squeeze when it comes to making decisions on accurate information, especially when it comes to client portfolios.

Even some of the best data providers in the world have not solved this problem, they are mostly at the mercy of the data they are provided with, which has very little consistency from firm to firm. Maintaining an accurate look-through is about having confidence in your decision-making. When you know the data is right, the conversation changes. You spend less time questioning the output and more time understanding the portfolio.

The One-Off Epidemic

A single portfolio review can be helpful, it's better than none, but it rarely solves anything on its own. Portfolios are constantly evolving. Underlying positions change incrementally, and market movements simply shift weights. Without a consistent review cadence, it is very easy for those changes to go unnoticed. Most providers sit you down, walk you through a few charts, point to where their product fits, and send you on your way. It's a common approach, but we think it leaves gaps.

In our case, our portfolio review comes through a quarterly cadence. Not because it leads to constant changes or there are drastic new insights, but because it gives a clearer understanding of how the portfolio is evolving, with the benefit of idea sharing. We pair that portfolio discussion with a macro presentation. Our positioning does not happen in a vacuum, there is always a reason behind it. Whether it's tied to market dislocations, a shift in macro events, or a swing in capital allocation flows. Connecting the portfolio back to the broader outlook helps determine if you are actually allocated to how you see the world.

Final Thoughts

Portfolio reviews should go beyond confirming that everything looks fine and instead improve your understanding of how the portfolio is actually positioned and evolving. Looking at your own portfolio will always be the starting point, but there is real value in stepping outside of that and adding an extra level of clarity that is difficult to achieve in isolation.

Our approach to portfolio reviews is built around that idea. We focus far less on back tested performance and more on underlying asset allocation. The goal is to look forward, not backward, and ensure that the portfolio today reflects your view for the future.

You can find a sample of our portfolio analysis here, and if you are interested in going through a review of your own model, feel free to reach out here.

— Brett Gustafson is an Associate Portfolio Manager at Purpose Investments

Sources: Charts are sourced to Bloomberg L.P.

The content of this document is for informational purposes only, and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold, or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable, however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees, and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain statements in this document are forward-looking. Forward-looking statements ("FLS") are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as "may," "will," "should," "could," "expect," "anticipate," intend," "plan," "believe," "estimate" or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on the FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.