Making a trade in your portfolio gives a portfolio manager a sense of purpose. It is the action that we believe we are paid a fee to do. Those trades usually feel clearer on the day they are made than they do months later. You have spent time on the rationale for both the buy and the sell, and you complete the trade across your models. Either the market has created some sort of pressure or opportunity, and the trade feels like a reasonable response to that moment.

However, after that trade, the market does not stand still, and the story can change. Your original thesis can be more difficult to remember over time. If markets run, a sensible decision can look too cautious, or if volatility fades, a trade that was designed to reduce risk can look unnecessary.

After attending a conference in Chicago this past month, Will Danoff, the legendary manager of the Fidelity Contrafund, brought some great tips and suggestions for the portfolio managers in the room. He was asked what he believed is the number one tip for managers. His answer? Keeping a trade journal for every trade you have ever done. He discussed the importance of documenting why a portfolio change was made before the outcome is known and having the ability to reference it in the future.

New tasks can be daunting. When adding another task to a role, we have to be setting out to solve a problem. The problem in this sense, when it comes to reviewing portfolio decisions, is that memory is not usually reliable, complicated by hindsight bias. If the trade worked, the original rationale can feel quite obvious in retrospect. When it doesn’t, so do the risks.

The tricky thing is that most portfolio decisions are made with incomplete information. There is always some level of uncertainty, but you have your thesis for filling in some of those gaps, or you believe so at the time. When a trade is maturing, the outcome becomes a little clearer, but the original environment for the trade begins to fade away.

A trade journal helps by freezing that rationale in time. It creates a more honest record of what the team felt at that point. A trade can make money for bad reasons, and it can lose money for good reasons, and sometimes it doesn’t have anything to do with your original thesis. If the only thing we review is the final return, we miss a lot of the lesson.

What Should Go in the Journal?

The trade journal should be simple enough so that the thought of it is not part of a daunting process. Over time, if it is too much work, it will likely be forgotten. Journaling can be tedious, but in the moment when the rationale is already in your head, jotting it down should be rather simple. The goal is to make sure every trade has to explain itself before it enters the portfolio. Think of it as the password to enter.

At a minimum, the journal should capture the action, the rationale, any risks on the horizon, and some sort of review point. That should be enough to capture a useful record without turning it into a research report.

|

Journal Field |

Questions to Answer |

|

Trade Action |

What changed in the portfolio? |

|

Rationale |

Why are we making this change

now? |

|

Funding Source |

How are we funding the trade? |

|

Risks |

What would tell us that we are

wrong? |

|

Review Trigger |

At what level should this

trade be revisited, both upper and lower levels? |

|

Postmortem |

What did we learn? |

Every team will have their own language or process, but the ultimate purpose should be the same. To create a record of the decision while the thinking remains fresh in your mind.

How We Use it

Within our process, we have the ability to tag trade notes directly to the security that is being traded. This allows us to visually see where decisions were made throughout the lifecycle of an investment. Instead of looking back and trying to guess or remember why a trade happened, the note sits directly on the chart. This is not possible for everyone, but a simple notebook also does the trick. Even your most frequently used AI companion can now be a good solution for keeping a historical track record of your trades.

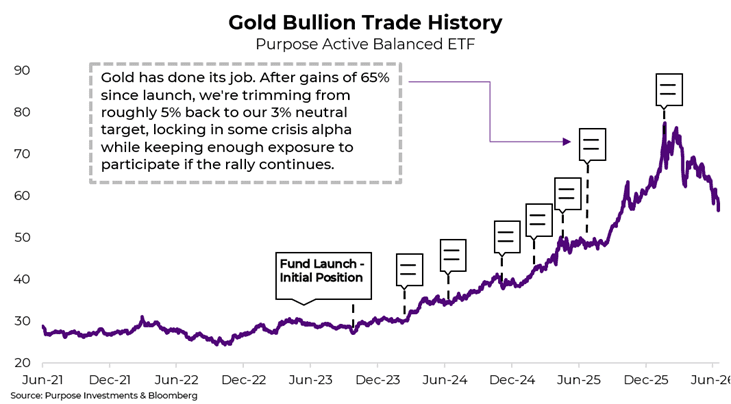

Below is a sample of what that looks like on one of our more frequently traded positions, gold bullion. Gold has been much more volatile recently than it has been in years past, and there are many lessons that can be learned along the way. At first glance, that April 2025 trade looks unfortunate. Bullion continued to move materially higher after we trimmed our position. Looking only at the price chart, it would be easy to say the trim was early or that we should have just let the position run.

That is why every bit of added context here is important. We launched our multi-asset portfolios 1.5 years prior to that trade, and since then, gold had gained roughly 65%. The concentration in the portfolio had grown to about 5%, off our baseline of 3%, which is a fairly meaningful overweight in the multi-asset space. We liked gold, we still do, but not that much.

It would have been very challenging to forecast an even greater sentiment shift toward gold. But for the sake of this, let's say we did, the sizing question is still important. Did we really want the concentration to move to 6% or 7% of the portfolio? At what level of the portfolio does gold stop being a diversifier and start becoming one of the main drivers of the risk in our portfolio?

Hence the trade journal, it separates the market outcome from the portfolio decision. The trade shows we were early, but the journal provides context around sizing, concentration and previous history.

Final Thoughts

Hindsight bias is a challenge, decisions looked back on can look cleaner than they felt in the moment. With a journal, that moment is preserved. Over time, the journal becomes less about any individual note and more about the pattern. It reveals whether trades have been tied to a consistent process, what factors are considered and some structure around your enter/exit discipline. Instead of looking back and guessing, the team can understand the actual thought process.

For advisors, the major benefit is a simple one. It creates a strong connection between the portfolio decision and the client conversation. Most clients won’t concern themselves with trades of the past, but there will be a few that will, and having the journal ready for those interactions can only benefit you.

The trade itself is only one part of the process, remembering why you made it is where a lot of the learning happens.

— Brett Gustafson, Associate Portfolio Manager at Purpose Investments

Sources: Charts are sourced to Bloomberg L.P. as of June 26, 2026

The content of this document is for informational purposes only, and is not being provided in the context of an offering of any securities described herein, nor is it a recommendation or solicitation to buy, hold, or sell any security. The information is not investment advice, nor is it tailored to the needs or circumstances of any investor. Information contained in this document is not, and under no circumstances is it to be construed as, an offering memorandum, prospectus, advertisement or public offering of securities. No securities commission or similar regulatory authority has reviewed this document and any representation to the contrary is an offence. Information contained in this document is believed to be accurate and reliable, however, we cannot guarantee that it is complete or current at all times. The information provided is subject to change without notice.

Commissions, trailing commissions, management fees, and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated. Certain statements in this document are forward-looking. Forward-looking statements ("FLS") are statements that are predictive in nature, depend on or refer to future events or conditions, or that include words such as "may," "will," "should," "could," "expect," "anticipate," intend," "plan," "believe," "estimate" or other similar expressions. Statements that look forward in time or include anything other than historical information are subject to risks and uncertainties, and actual results, actions or events could differ materially from those set forth in the FLS. FLS are not guarantees of future performance and are by their nature based on numerous assumptions. Although the FLS contained in this document are based upon what Purpose Investments and the portfolio manager believe to be reasonable assumptions, Purpose Investments and the portfolio manager cannot assure that actual results will be consistent with these FLS. The reader is cautioned to consider the FLS carefully and not to place undue reliance on the FLS. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise FLS, whether as a result of new information, future events or otherwise.