Thought that title may have gotten your attention.

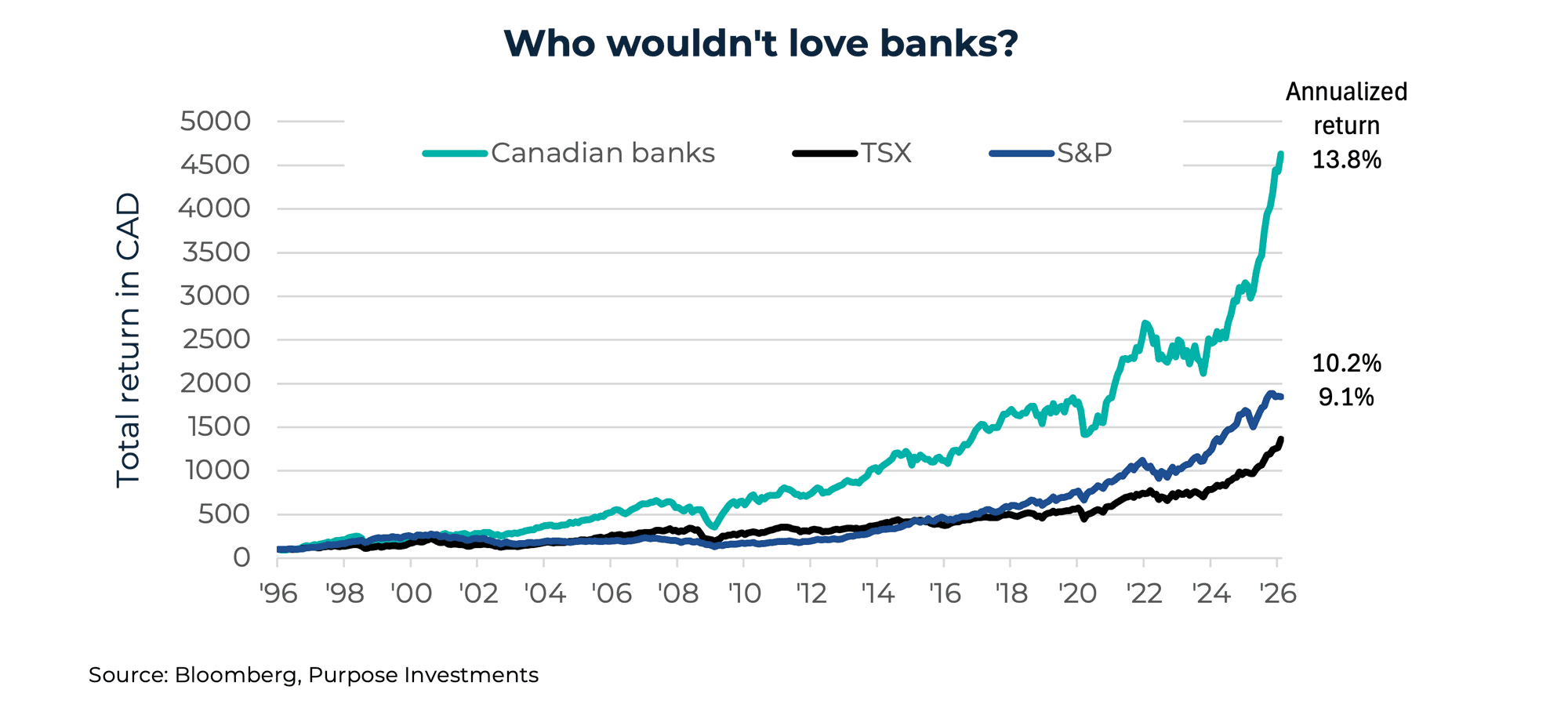

To be clear, we’re talking about the epic performance run of bank stocks over the past decades, not a rush of customers trying to get back their deposits. Over the past 30 years, Canadian banks have earned annualized returns of 13.8%. That’s better than the overall S&P/TSX Composite Index at 9.1%, and even better than the almighty S&P 500 Index at 10.2%. It’s little wonder Canadians have a soft spot in both their hearts and portfolios for Canadian banks.

Last year, too, banks crushed it, growing 45% based on S&P/TSX Banks index. Sure, gold got most of the attention for helping drive the S&P/TSX Composite Index to an overall 30% gain for 2025, but banks deserve about equal credit.

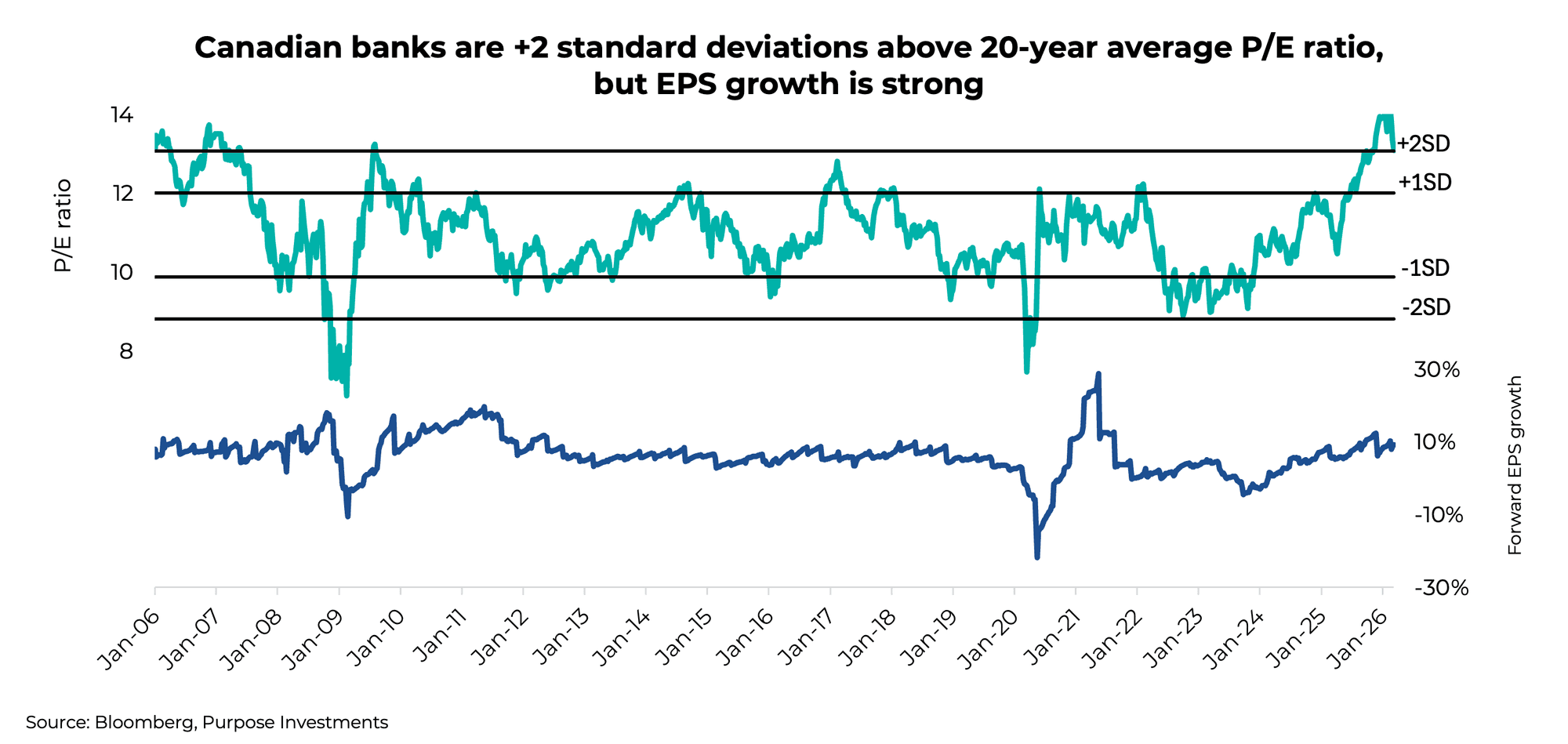

Here’s the challenge, though: bank valuations have certainly been pushed higher. The chart below is the Canadian bank index over the past 20 years. The price-to-earnings ratio was 14x in February, but it has moderated down to 13.1x today. For the banks, that’s pretty pricey.

Valuations are just one part of the story, as earnings growth somewhat justifies the higher valuations. Earnings estimates have been on the rise for the banks, and current forecasts have earnings growing at just under 10% looking out over the next 12-month period. Still at 13.1x, investors are certainly paying up for this growth.

Banks are feeling some tailwinds that have driven share prices higher. Net interest income is strong thanks to higher yields, and loan losses remain contained. Plus, capital markets and wealth are doing well, while housing and real estate are a bit of a laggard. With the rise in share prices, how much of the good news is already priced in? It appears a healthy amount.

Insurance Companies: Better Value?

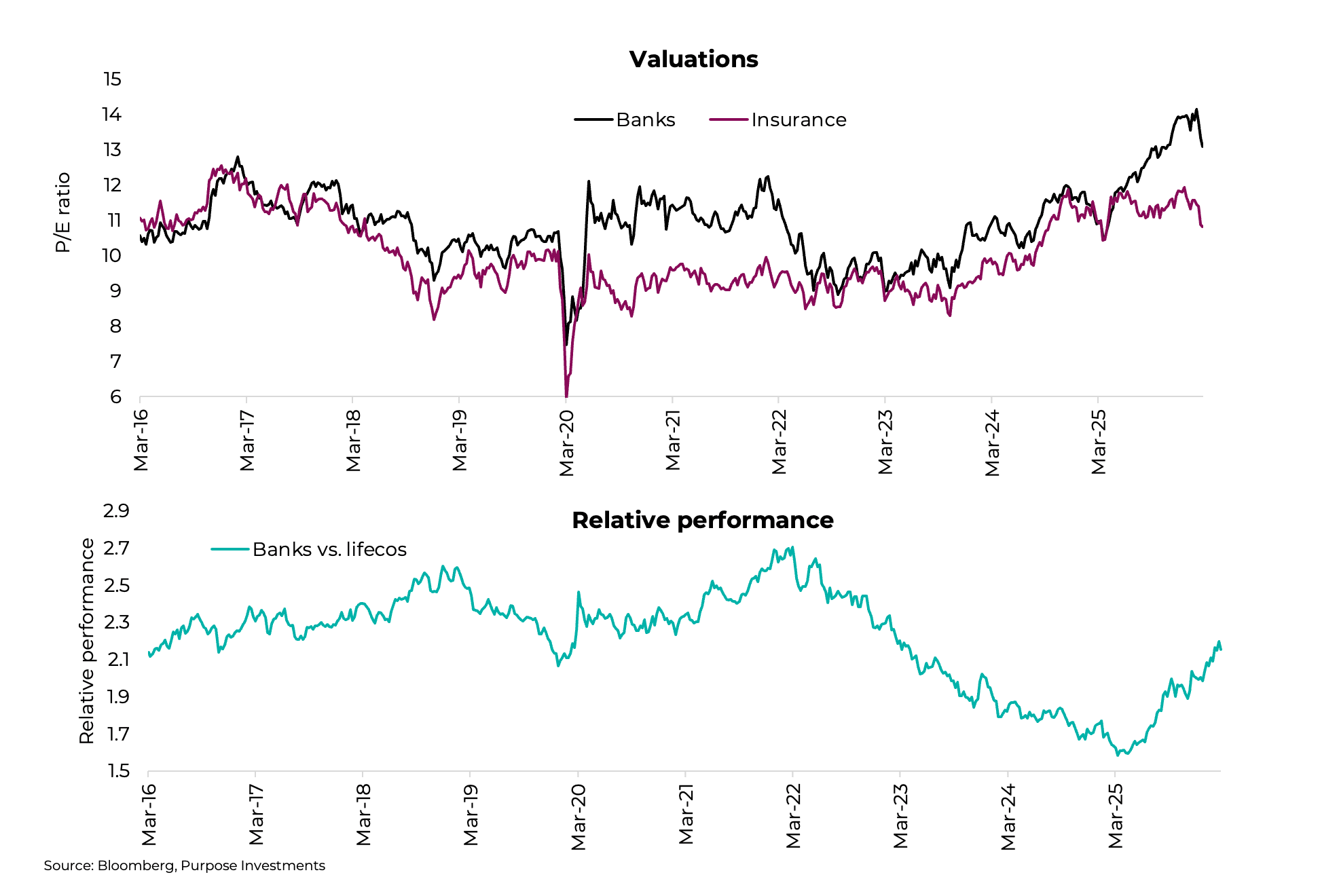

There does appear to be better value elsewhere in the Canadian Financials sector. For the S&P/TSX Composite Index, Financials carry a 31% weight: 21% is banks, and the remainder is split between insurance and capital markets. Of interest is the valuation spread between banks and insurance.

The stronger relative performance of the banks compared to the insurance sub-indices for the S&P/TSX Composite Index has led to a rather high historical valuation gap. Insurance companies may not be cheap on an absolute basis, but they certainly offer better value relative to banks, and many of the underlying insurance companies have similar growth profiles.

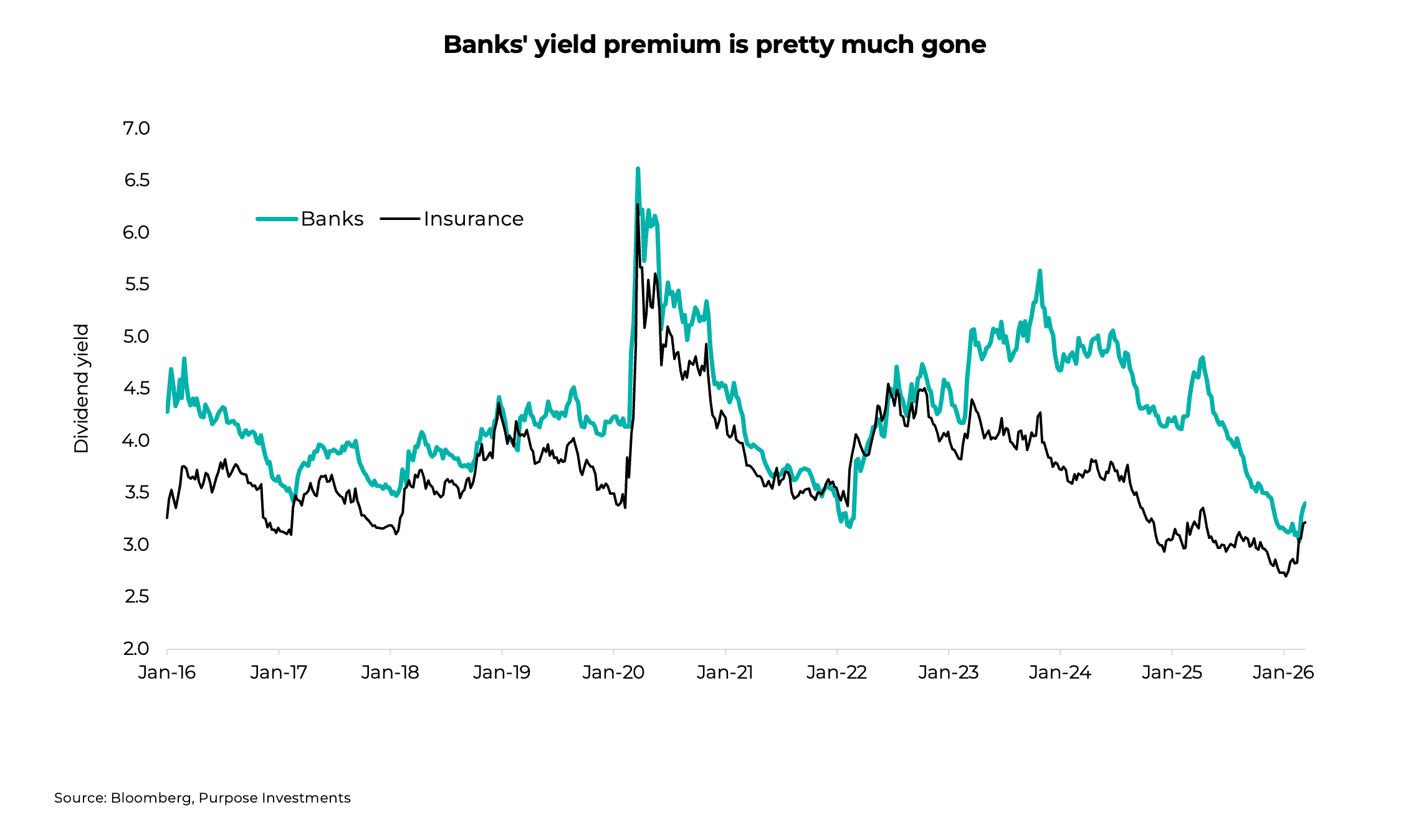

For those who value dividends — hopefully all of us, because we are Canadian after all — the higher dividend yield offered from banks appears to have almost disappeared relative to insurance.

Final Thoughts

Obviously, Canadian portfolios pretty much always have some exposure to banks; they’re simply such a big part of our market. The dividends are also an attractive attribute. Plus, the insurance space has historically been a bit higher beta. But given valuations, growth and current dividend yields, we’re a bit more positive on insurance and a bit more cautious on the banks.

Craig Basinger is the Chief Market Strategist at Purpose Investments