Every summer, a group of lucky Torontonians make the odd weekend pilgrimage to cottage country. For those less familiar, it’s about a two and a half hour drive north of the city, up Highway 400 North, continuing on either Highway 11 or staying on the 400 en route to Parry Sound.

On the other side of this drive is nirvana. Here you will find tranquil lakes lined with trees, the calls of loons echoing across the bay, and perhaps your beverage of choice on the dock if you feel so inclined.

When you go here – you think to yourself, this is it. This is the end game. Meticulous planning to arrive at the ultimate destination has paid off.

Also on this drive, just as you get about forty-five minutes north of the city, is the amusement park – Canada’s Wonderland. At this location of metal mayhem, you’ll find rides like the Drop Zone (which is exactly what it sounds like), the towering twisting coaster called the Leviathan, and also several merry-go-rounds.

Now stay with me on this analogy.

The market right now is taking a mandatory pitstop at Canada’s Wonderland en route to the cottage. The cottage is the end state: earnings growth, innovation, productivity, lower rates over time, and the quiet satisfaction of owning great businesses through a full cycle. That is the destination everyone signed up for. But, instead, you have to stop at Wonderland.

The Drop Zone is the sudden drawdown that arrives during a momentum unwind. The Leviathan is the crowded AI trade, climbing higher and higher until the entire market seems to be strapped into the same seat, moving at the same speed, with everyone pretending they are comfortable. The merry-go-round is sector rotation: investors cycling from semis to defensives, from growth to value, from small caps to mega caps, and then back again, often with very little changing in the underlying long-term thesis.

The key is recognizing which ride you are on (maybe all three?!) and keeping in mind that the dock is still there waiting.

Enough with the prose – let’s talk markets.

When the Facts Change, I Change My Mind. The Facts Have Not Changed (Yet).

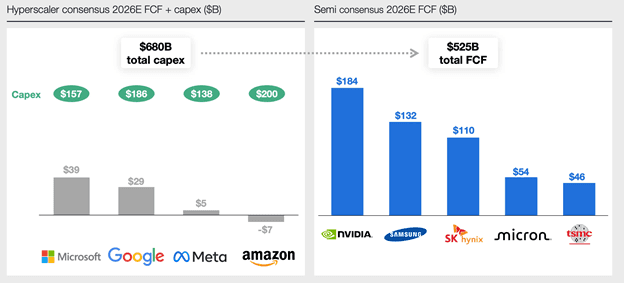

The belle of the ball this year has been semiconductors by a mile. On a YTD basis, The SOXX went from pretty close to flat at the end of March, to up 104% two months later, by July 3. It has since retraced significantly. The narrative went a little something like this: AI adoption is rapidly accelerating, and we are structurally undersupplied on compute infrastructure. Bottlenecks create pricing power. Semiconductors + infra are the rotating bottlenecks. Hyperscalers are seeing such large demand that they keep moving Capex numbers up. Hyperscaler Capex = semiconductor free cash flow.

Source: Coatue

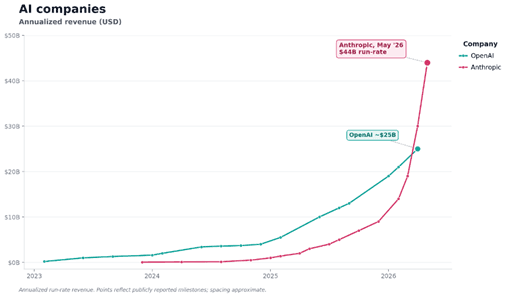

The other narrative driver is what I am now officially naming the “Anthropic Explosion” (in a good way). Anthropic’s annualized revenue run (ARR) rate went from $1B at the end of 2024, to $9B at the end of 2025, and then it put on THIRTY SIX BILLION more over five months to hit $45B in May.

Source: The Information

To put that into context, Anthropic added more ARR in the first five months of 2026 than Salesforce, ServiceNow, Snowflake, Databricks, CrowdStrike, Shopify, Adobe, and Palantir typically add in a year combined.

Anthropic’s CRO then jumped on a podcast and told the market that they had net revenue retention (NRR) rates of 500%. NRR is a metric that measures the percentage of recurring revenue retained from existing customers over a specific period, factoring in upgrades, downgrades, and cancellations. The average NRR of the companies listed in the previous paragraph is 130%... Anthropic is at 500%?

So now we have our revenue proof point. So party on, right?! Not so fast.

Then we turned the monthly calendar to June and we started to get these headlines:

· “AI sticker shock hits corporate America” Axios

· “Microsoft starts canceling Claude Code licenses” The Verge

· “Mystery company accidentally blew $500 million on Claude AI in a single month — failed to put usage limit on licenses for employees” Tom’s Hardware

· “Anthropic tightens Claude limits and OpenAI courts defectors” Axios

· “OpenAI Considers Drastic Price Cuts, Anticipating Costly War For Users With Anthropic” Wall Street Journal

The narrative completely switched. When you get all of these headlines, people start to actually worry how much they are spending, and there starts to be a doubt cast on the return that companies are getting for all this AI spend. When you have cancellations or retreatments en masse, you also see that NRR figure start to retreat because now, all of the sudden, we start to see churn. The market has never seen these things before so we have no idea how sticky some of this revenue actually is. Is it truly recurring revenue?

There has been a trend going on called tokenmaxxing, which is when you see employees bragging about how many credits they have used, even if it is for entirely useless applications they are building. It turns out that running agent loops so your boss thinks you are AI-pilled ends up being pretty expensive. It got so bad that some companies had leaderboards and handed out awards to whoever spent the most tokens. This reminds me of Goodhart’s law which states, "When a measure becomes a target, it ceases to be a good measure." These leaderboards do not solve for the right objective, which is enhanced productivity. Token usage is not a good measure of output for a digital worker. The end product is.

When you draw all of this out, the natural conclusion is that the market has switched to not recognizing real value. As a result, companies will right-size their cost structure, stop pulling so much growth forward, and all of this demand will evaporate. Semis will be sold off. But this is the wrong conclusion.

What the Market is Missing

All of this tokenmaxxing in the early days was really just used to increase adoption rates amongst employees. Do you know how hard it is to teach an old dog new tricks? Just ask anyone who has run a Salesforce integration. The average Fortune 500 company implements Salesforce in 12 to 24 months. Complex global transformations can take 24 to 36+ months. THREE YEARS to implement salesforce… No wonder why some companies just encourage this to drive adoption.

The next step is optimization. There have been excellent posts for how to manage runaway token cost. These include model routing (choosing a cheaper model for simpler tasks), prompt caching (storing content so repeat calls cost ~90% less), AI cost visibility and reporting, batch APIs (grouping together non-urgent asynchronous tasks), and employee education.

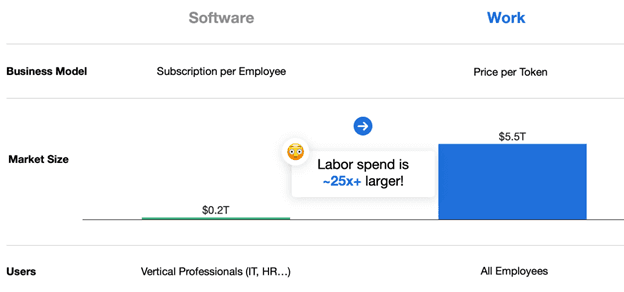

But optimization does not necessarily mean growth collapses for AI companies. As employees find more and more use cases, at cheaper token costs, they will use more AI, likely causing a net increase overall – a Jevons paradox redux. Additionally, the TAM is not the software budget. It’s the labour market. Coatue has an excellent slide on this:

Source: Coatue

The Real Red Flags

The real threat here to frontier LLMs (Google, Anthropic, OpenAI) is open weight models. The thesis goes, that as open source/weight models get better, commoditization will drive down prices. I think this is a credible bear thesis. However, the frontier models are just so much better than the alternative and (for now) they will continue to be priced at a premium. Sure, there will be routing to cheaper models, but for the harder questions, you need the higher intelligence model. Frontier companies keep pushing this envelope forward, and as they continue to do so, they can still command a premium. Time will tell how long this competitive advantage lasts, but even if it commoditizes, guess what? You still need more compute for inference. Semiconductors don’t care who wins the model race. All roads lead to more compute.

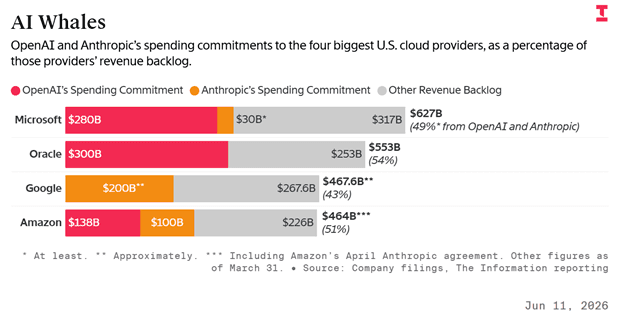

However, we still need to worry about the circular revenue/bookings problem. A larger portion of cloud companies’ backlog/bookings is now made up of frontier LLM bookings. If the unit economics cracks on the frontier level, the level of committed spend going from OpenAI and Anthropic to the hyperscalers starts to rightfully get questioned. Those hyperscalers are the #1 customers for semis. I think that’s also a credible and very real bear case.

Source: The Information

I think another critical point will be when frontier LLMs file their S-1s. With Anthropic and OpenAI now both filing to go public, the market will get a look at actual audited financial statements. It’s going to be very important that we see continued acceleration of revenue, but also gross margin profiles that make sense. Any fallbacks with these guys will echo throughout the ecosystem.

For now – the thesis is still intact. Anthropic’s revenue run rate is seeing fantastic growth, Open AI is still growing with significant upside if they can actually figure out ads, and the hyperscalers themselves are also integrating their own models. I will be writing a full piece that covers all aspects of circularity from bookings, revenue, and particularly financing when it comes to the chip side. For now, this is a virtuous flywheel, but it increases the risk of a large-scale shockwave as the system becomes more interconnected.

So now that I’ve covered the shifting narratives around adoption and usage, let’s go into the key debate right now in semis.

Cyclical vs. Structural

The core debate in the semiconductor Twitter (X) wars is whether semis have finally evolved from cyclical commodities to structural growers. There are good points on both sides of this one.

The case for cyclical is that every period of undersupply eventually ends in a glut. This thesis highlights that semiconductors are still a supply-driven capital cycle with volatile pricing. High margins attract capacity, capacity arrives with a lag. By the time fabs, packaging lines, and memory capacity come online, demand may have pulled back, creating a glut, down go prices and with them margins. Rinse and repeat.

The case for structural is that AI turns compute into a recurring input to economic production. In the PC and smartphones eras, semiconductors were tied to device replacement cycles. One person would have so many devices, replace them ever so often, layer on population growth, and that’s pretty much the market. In the AI era, semiconductors become the raw material for training, inference, agents, code generation, robotics, drug discovery, simulation, and data center expansion. There is a finite amount of people, but an infinite amount of agents. This makes the demand pool larger and more persistent than a normal consumer electronics cycle.

The best answer is: semiconductors have become a structural growth sector with cyclical earnings power. The long-term revenue base is moving higher because AI increases semiconductor intensity per dollar of GDP. However, the path will still be violent because supply comes in discrete chunks, customers over-order when capacity is scarce, memory pricing overshoots in both directions, and equity markets tend to extrapolate the most recent margin regime.

For portfolio construction, I would not treat all semis as one factor anymore. The old framework was “buy semis early cycle, sell semis late cycle.” The new framework is more layered:

· Own structural bottlenecks through cycles: leading-edge foundry, advanced packaging, HBM leaders, critical equipment, networking silicon, power/data center enablers.

· Trade the cyclical parts with discipline: memory, analog, mature-node foundry, consumer-exposed chipmakers, and second-derivative equipment names.

· Be most careful where structural narratives meet peak pricing: HBM, WFE, AI server supply chain, and any company where 2026 or 2027 earnings are being treated as a new permanent baseline.

How to Position

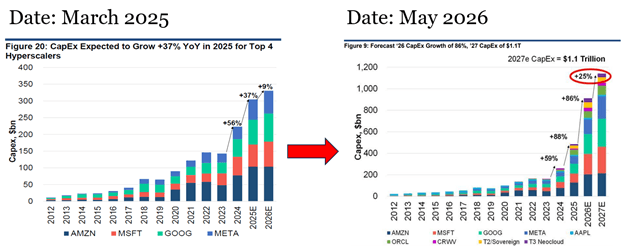

Think about the next three years but position your portfolio around the next 12 months. I think you genuinely have to have a framework on what the world looks like three years from now and where you could see different scenarios going. However, everything is changing so fast, trying to forecast anything beyond a year seems futile when it comes to earnings. Just look at capex estimates on a YoY basis. Frequent readers will recognize this chart. The street was off by over HALF A TRILLION DOLLARS in incremental capex in 2026 that all went to semis. I think the street will be off again for 2027 as goalposts move out.

Source: Evercore ISI, Mark Lipacis

So listen to what the market is telling you is going to happen. I’m going to switch from the usual baseball analogy to a soccer one because it’s World Cup season. I think we are in halftime right now. We are still compute constraint, unit economics are still accelerating, and we still have plenty of funding mechanisms for 2027 capex numbers to go up (re: Google issuing $80B!!! in equity).

Wrapping Up

We are smack dab in the middle of the largest mobilization of capital in human history. Bigger than railroads, the Manhattan project, telecom, and the shale revolution. You cannot afford to sit out the life-changing value creation that we are seeing in the stock market right now. We are seeing intelligence itself being metered and sold to the masses, which is fundamentally altering the way we think about unit economics within businesses and macroeconomic theory as data centers (capital) enable digital agentic workers (labour).

But you also have to have your wits about you. I know this may sound morose, but nothing is ever as good or as bad as it seems. So we need to take heed of the words from the songbirds of my generation:

Nothing lasts forever.

I'm sorry I can't be perfect”

— Simple Plan

Strong Convictions. Loosely Held.

— Nicholas Mersch, CFA